Sentora PRIME and the next phase of RWA vault curation

A new Morpho vault has recently launched around PRIME, bringing Hastra’s HELOC-backed yield asset into Ethereum’s lending ecosystem with risk curation from Sentora.

The launch is not only about giving users another source of yield. It also shows how RWA DeFi is moving toward a more advanced model, where the focus is no longer just on bringing assets onchain, but on defining how those assets are used, priced, and risk-managed inside lending markets.

This article explores how PRIME works, why its Morpho launch matters, and how Sentora’s approach to vault curation reflects the next phase of RWA adoption.

Ethereum’s search for uncorrelated yield

Stablecoins have long been a primary source of yield on Ethereum through lending; however, stablecoin yields are no longer proving to be as competitive. As stablecoin yields have gone down, the top 10 largest stablecoin yield sources now average between 4.31% and 2.50% APY.

With the Effective Federal Funds Rate at 3.63%, users are no longer being adequately compensated for the risks they take by locking funds into smart contracts. In many cases, they could earn a similar return through lower-risk alternatives such as money market funds, Treasury bills, or other traditional cash products.

This changes the value proposition for DeFi yield. When stablecoin lending rates were meaningfully higher than traditional rates, users could justify the additional smart contract, liquidity, and counterparty risks. But when onchain stablecoin yields sit close to risk-free rates, the risk premium starts to disappear.

This has created a search on Ethereum for yield sources that are less correlated to crypto lending markets. In the current landscape, crypto-native assets have not been able to provide enough competitive yield on their own.

The idea behind PRIME

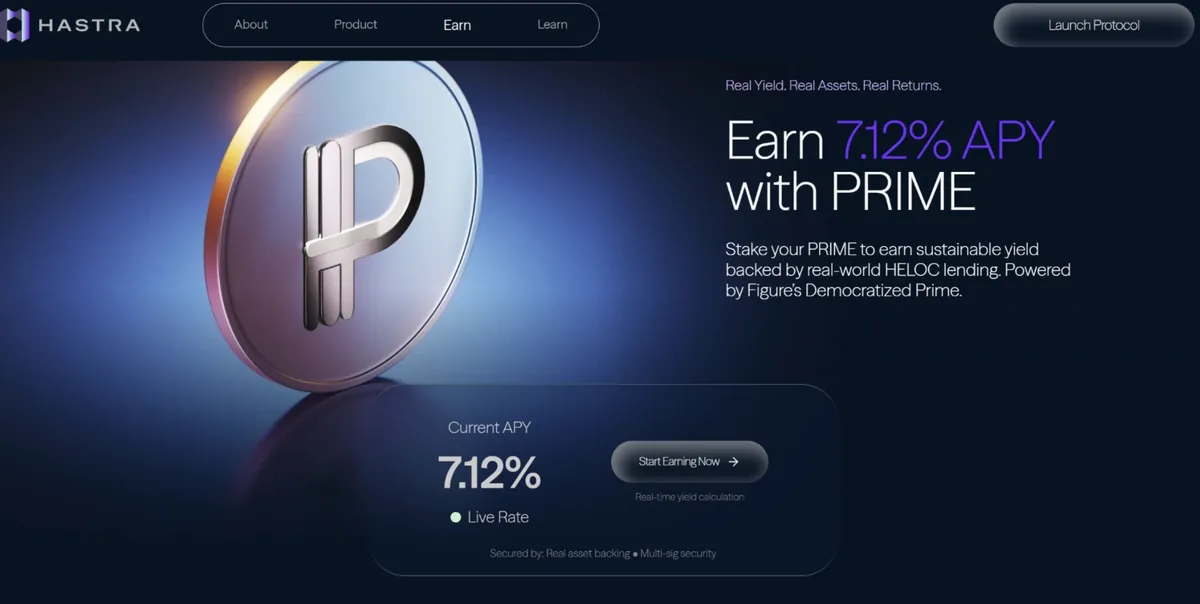

One of the assets providing an alternative to stablecoin yield is PRIME, issued by Hastra, which brings exposure to a real-world credit market into DeFi.

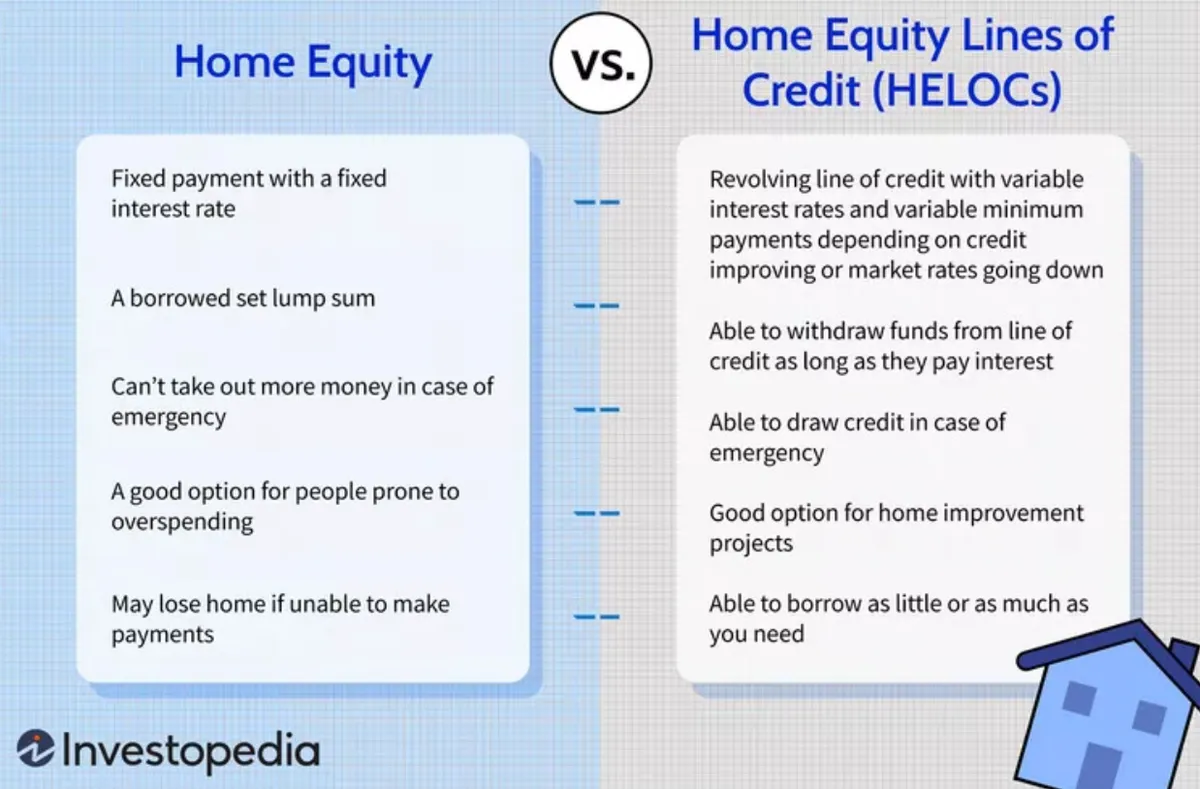

To understand PRIME, it is first important to understand the market it gives users exposure to. PRIME is built around home equity line of credit loans, or HELOCs. A HELOC is a form of consumer credit where a homeowner borrows against the equity in their home. The borrower receives access to a revolving credit line, while the loan is secured by the value of the home.

In practice, this means PRIME is not simply exposure to home equity itself. It is exposure to credit backed by home equity.

PRIME tokenises exposure to this lending activity. It represents a deposit into Democratized Prime, a warehouse lending facility for Figure-originated HELOCs that are waiting to be securitised and sold to institutional buyers.

During this period, capital is lent against performing HELOCs, and PRIME holders earn yield from the lending spread created by those operations, with the APY currently sitting at 7%.

This makes PRIME different from most DeFi yield products. Its return does not come from token emissions, trading fees, or demand for crypto-native borrowing. Instead, it comes from real-world lending activity backed by home equity credit.

That gives PRIME a return profile that is harder to replicate with purely crypto-native assets. Stablecoin lending, staking, and liquidity provision are all closely tied to onchain activity. When crypto markets slow down, those yields often compress. PRIME is different because its yield is driven by borrowers paying interest on HELOCs, not by DeFi leverage cycles.

The collateral pool is backed by the unpaid balances of performing HELOC loans, discounted at an advance rate. Loans that become 60 or more days delinquent are removed from the collateral pool. This creates a yield source linked to real-world credit performance rather than crypto market sentiment.

How to Access PRIME

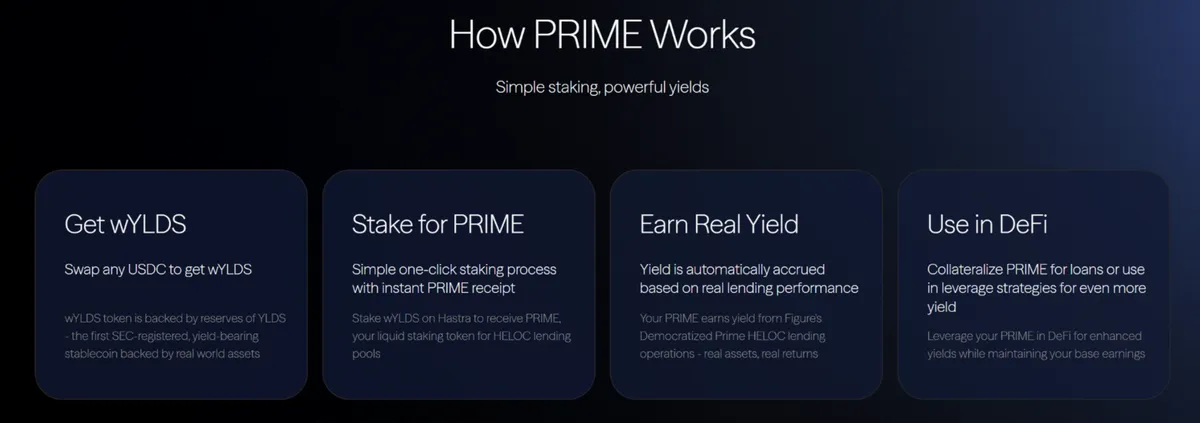

Users can access PRIME by first acquiring wYLDS. wYLDS is a token backed 1:1 by YLDS, a yield-bearing stablecoin backed by real-world assets, with yield distributed to wYLDS holders automatically.

After acquiring wYLDS, users can stake it on Hastra to receive PRIME. PRIME then acts as the liquid staking token for the HELOC lending pool, allowing users to earn yield from Democratized Prime’s lending operations while keeping the token usable across DeFi.

Once users hold PRIME, they can simply hold it to earn yield or use it in DeFi. This allows PRIME to function as both a yield-bearing asset and a collateral asset, giving users exposure to real-world credit while maintaining onchain liquidity and composability.

Sentora launches PRIME vault on Morpho

While PRIME has been live on Solana since December 2025, where it has seen strong DeFi traction through Kamino and amassed a market of $300 million in TVL, it has now also gone live on Ethereum through its newly launched lending market on Morpho in partnership with Sentora.

The Morpho vault allows Ethereum users to lend against PRIME through a more structured vault product. This is important because Ethereum remains the largest DeFi liquidity environment. Bringing PRIME to Morpho gives the asset access to a deeper base of stablecoin capital, while giving Ethereum users exposure to a yield source that is not directly dependent on crypto-native leverage cycles.

How the Morpho vault works

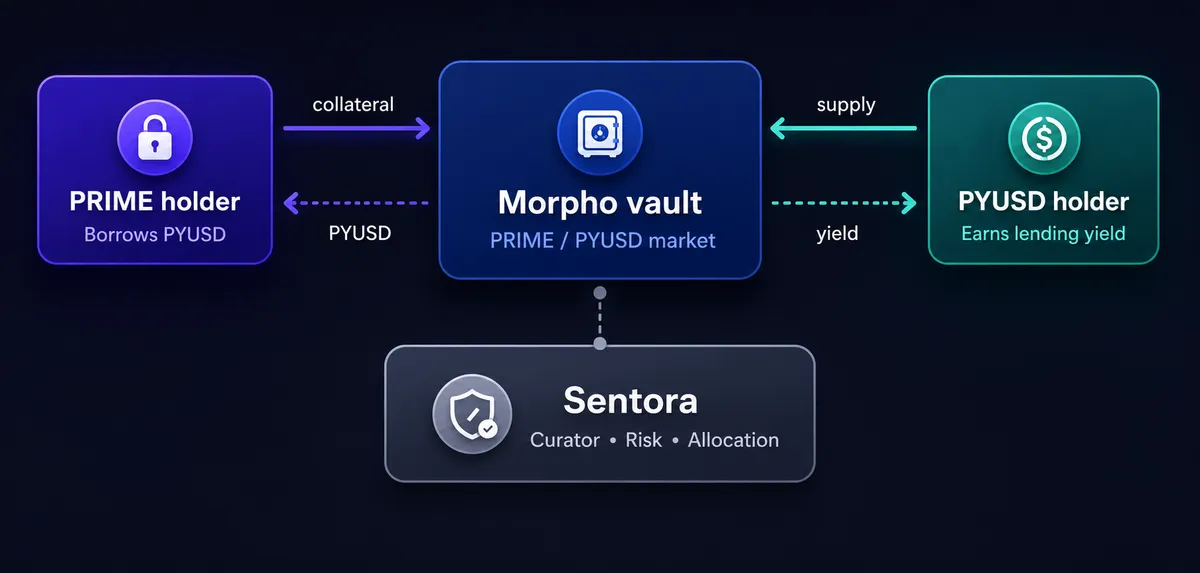

The Sentora PRIME Main vault creates a lending market between PRIME holders and PYUSD holders.

For PRIME holders, the vault makes it possible to borrow PYUSD against their PRIME. Instead of selling PRIME, they can use it as collateral and access stablecoin liquidity while keeping exposure to the underlying HELOC-backed yield asset.

For PYUSD holders, the vault creates a way to earn yield by lending against PRIME collateral. They are not directly buying PRIME or taking direct exposure to the token. Instead, they supply PYUSD into a curated lending market where PRIME is used as collateral.

Sentora acts as the curator that manages how stablecoin liquidity is allocated, monitored, and exposed to PRIME-backed markets.

This structure creates two different ways to participate in the same market. PRIME holders can unlock liquidity from their position, while PYUSD holders can earn lending yield from borrowers using PRIME as collateral. Sentora’s role is to curate the vault, manage allocation, and monitor the risk parameters around how PYUSD liquidity is exposed to PRIME-backed borrowing.

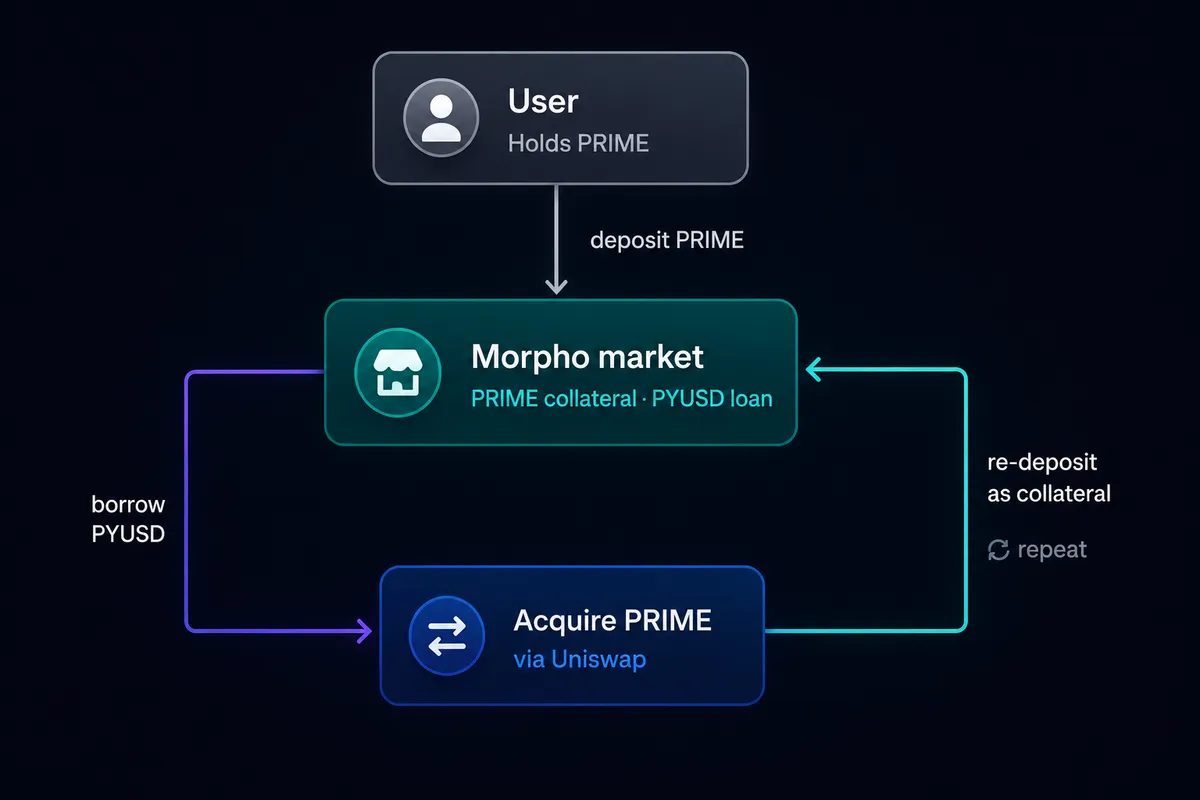

The looping opportunity

The structure of the PRIME/PYUSD market creates a compounding yield strategy that is worth examining in its own right. Because PRIME is a yield-bearing token, meaning its value accrues over time in the same way as assets like wstETH or sUSDe, it can be used as the basis for a leveraged loop.

The mechanics work as follows. A user deposits PRIME as collateral into the Morpho market, borrows PYUSD against that position, uses the borrowed PYUSD to acquire more PRIME, and then deposits that additional PRIME back into the market.

Each loop amplifies exposure to PRIME's underlying HELOC yield while adding a proportional borrowing cost on the PYUSD side. The net return at any level of leverage is determined by the spread between what PRIME yields and what it costs to borrow PYUSD on Morpho.

Position sizing and leverage

To see how this works in practice, consider a user who starts with $1,000 of PRIME. They deposit it into the Morpho market and borrow $860 of PYUSD against it, remaining within the 86% LLTV limit. They then use the borrowed PYUSD to buy more PRIME and deposit that PRIME back into the market.

At this point, the user has $1,860 in collateral and $860 in debt. Their net equity is still $1,000, but their PRIME exposure has increased to 1.86x their starting position. If the user repeats this process two more times, the position becomes increasingly leveraged.

Loop | PRIME collateral | PYUSD debt | Leverage | Health factor |

Start | $1,000 | $0 | 1.00x | — |

Loop 1 | $1,860 | $860 | 1.86x | 1.860 |

Loop 2 | $2,600 | $1,600 | 2.60x | 1.398 |

Loop 3 | $3,236 | $2,236 | 3.24x | 1.245 |

After three loops the position holds $3,236 in PRIME collateral against $2,236 in PYUSD debt, representing 3.24× the original exposure. The 7% yield now applies to the full $3,236, while the 3.38% borrow cost applies only to the $2,236 in debt.

That asymmetry is what makes the loop work: gross yield on the collateral side runs at 22.7%, against a blended borrow cost of 7.6%, leaving a net APY of approximately 15.1% on the original $1,000, more than double what holding PRIME unlevered would produce.

The health factor at loop 3 sits at 1.245, meaning collateral would need to fall by 24.5% before the position becomes liquidatable under stable price conditions. That buffer matters because Morpho liquidations are immediate and permissionless, with no auction delay, and any external party can liquidate a position that breaches the LLTV threshold within a single block.

As leverage scales up, so does the borrowing cost. The net return at each loop depends entirely on maintaining a positive spread, meaning PRIME yield must stay above the marginal PYUSD borrow rate on Morpho.

A look at the data

The PRIME launch on Morpho can be understood through two layers: the Sentora PRIME Main vault and the underlying PRIME/PYUSD lending market.

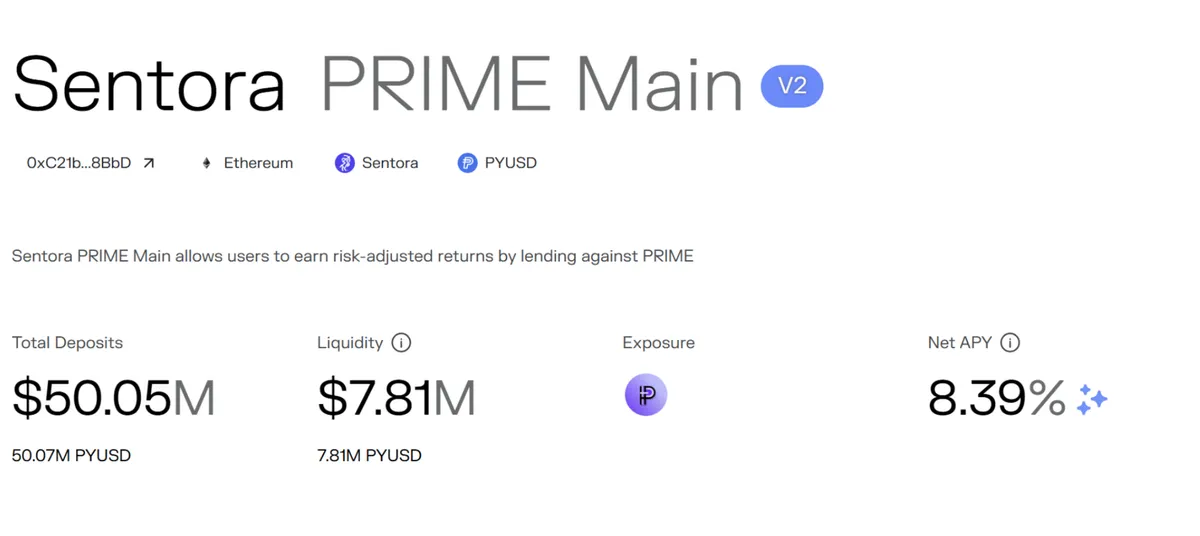

Sentora PRIME Main

The Sentora PRIME Main vault is the user-facing vault for PYUSD depositors. Users deposit PYUSD into the vault, and Sentora allocates that liquidity into PRIME-backed lending opportunities on Morpho.

At the time of writing, the vault has reached $50.05 million in total deposits, with $7.81 million in available liquidity and a net APY of 8.39%.

For a vault launched on May 8, 2026, this shows strong early demand from Ethereum users looking to earn yield by lending against PRIME collateral.

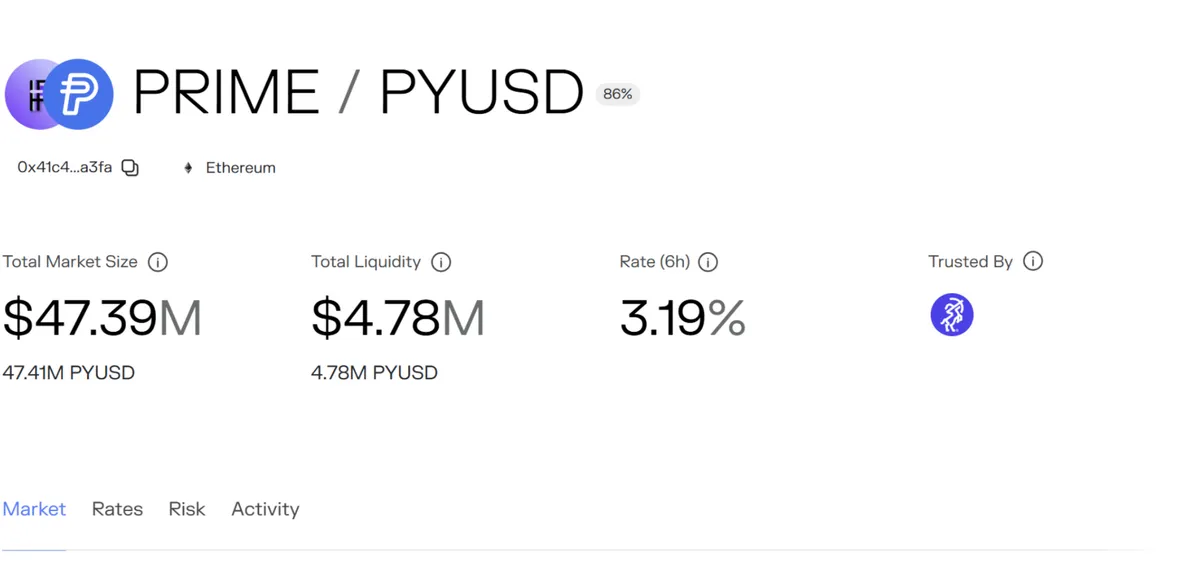

PRIME/PYUSD market

The underlying PRIME/PYUSD market is where the borrowing and lending activity happens. In this market, PRIME is the collateral asset, and PYUSD is the loan asset. The market currently has a total size of $47.39 million, with $4.78 million in available liquidity, showcasing strong and continued demand.

The PRIME/PYUSD market has an LTV of 86%, meaning borrowers can borrow against PRIME up to that threshold. Because the yield PRIME holders currently earn by holding PRIME is higher than the borrowing rate, borrowing against PRIME has proven attractive.

Utilisation sits at 89.9% at the time of writing, indicating that most of the supplied PYUSD in the market is being actively borrowed against PRIME collateral.

Separating asset risk from vault risk

What cannot be underestimated is the importance of Sentora’s role as a risk curator for this vault. The PRIME vault highlights a broader shift in RWA DeFi, where the market is moving from simple tokenisation toward risk curation.

Bringing an asset onchain is no longer the main challenge. The harder question is how that asset should be used once it enters DeFi, who should take the underlying asset risk, and how stablecoin liquidity should be protected around it.

This becomes especially important with RWAs such as PRIME. As RWAs move beyond tokenized Treasuries, the risk profile starts to change. Treasury products are easier for DeFi users to understand because the underlying asset is short-duration government debt.

Private credit is different. It can involve credit losses, liquidity constraints, duration risk, changes in buyer demand, and price movement during stressed market conditions.

Risk Area | Tokenized Treasuries | Private Credit |

Underlying asset | Short-duration government debt | Loans backed by real-world borrowers or collateral |

Main risk driver | Interest rates and duration | Borrower repayment, collateral quality, and liquidity |

Liquidity profile | Generally more liquid and easier to price | Can become harder to exit during stressed markets |

Yield source | Government debt yields | Lending spreads from private credit markets |

DeFi treatment | Closer to a yield-bearing stable asset | Requires more active risk curation |

This is the core difference behind Sentora’s approach. PRIME holders are exposed to the underlying HELOC-backed asset. PYUSD lenders are not buying PRIME directly. They are lending against PRIME collateral through a vault. These are related exposures, but they are not the same risk, which is why a risk curator should not treat them the same way.

The curator’s role is to define how much stablecoin liquidity can be exposed to the collateral, under what conditions, and with which protections in place.

In this model, RWA DeFi becomes less about simply listing new assets and more about designing the rules around how those assets can be used. Sentora is pioneering this role by showcasing how risk curation can be applied to more complex RWAs.

How Sentora manages PRIME’s risk surface

So let’s have a look at the risks that Sentora has identified and how it mitigates these risks through its risk curation..

The most important risk is extension risk. PRIME is built around a short funding window where HELOCs are expected to be securitized and sold to institutional buyers. If buyer demand weakens, PRIME could become exposed to the loans for longer than expected. This does not automatically mean losses, but it changes the nature of the exposure. A short-duration credit position can start behaving more like a longer-duration mortgage-backed position.

That extension can then create second-order risks. A longer holding period can make PRIME more sensitive to rates, credit spreads, and changes in liquidity.

Even if the underlying HELOCs continue to perform, the token can become harder to price or exit during stressed markets. This matters because PRIME is used as collateral in the Morpho market. If the collateral becomes more volatile, the vault needs enough protection through LTV limits, exposure caps, and liquidity buffers.

Aside from extension risk, there are also other risks, as identified in the table, that Sentora aims to mitigate through its role as a risk curator.

Risk | Why It Matters | How Sentora Mitigates It |

Extension risk | PRIME could shift from short-duration warehouse exposure into longer-duration mortgage-backed exposure if buyer demand weakens. | Models liquidity around extension scenarios and avoids assuming that loans will always exit on the normal timeline. |

Duration risk | A longer holding period can make PRIME more sensitive to rate changes and credit market conditions. | Uses conservative LTVs so the vault has more protection if collateral conditions change. |

Credit spread volatility | Private credit assets can reprice during stressed markets, even if loans continue to perform. | Maintains buffers between collateral value and borrowed stablecoin liquidity. |

Liquidity risk | PRIME may become harder to exit or price during periods of market stress. | Keeps vault parameters flexible and manages liquidity assumptions around stressed conditions. |

Bad debt risk | If collateral falls too much before liquidation, stablecoin lenders could take losses. | Prioritizes stablecoin depositor protection through LTV limits, exposure caps, and active risk controls. |

Sentora’s approach is to surface these risks at the vault level. Its platform monitors collateral quality, utilization ratios, and liquidity conditions around the HELOC exposure. When risk conditions change, Sentora can adjust parameters such as collateral factors, rate caps, and exposure limits.

By doing this, Sentora is not able to remove PRIME’s risk entirely. That would not be realistic for a private credit-backed asset. Instead, the goal is to separate the risk taken by PRIME holders from the risk taken by PYUSD lenders.

PRIME holders accept the asset-level risk of the underlying HELOC-backed exposure. PYUSD lenders are lending against PRIME collateral and should be protected by the vault’s parameters. What Sentora does in terms of risk management is make sure there are boundaries between those two groups, so stablecoin liquidity is not unknowingly taking the full risk of the underlying asset.

The next phase of RWAFi depends on curators

The launch of Sentora PRIME on Morpho shows how the RWA market is moving into a more mature phase. The first wave of RWAs was focused on access. Tokenised Treasuries gave users a way to hold familiar real-world yield onchain. PRIME pushes that idea further by bringing private credit exposure into Ethereum’s lending environment.

The next phase will depend on curation. Private credit cannot be treated like Treasury exposure, and RWA tokens cannot be treated as interchangeable collateral simply because they exist onchain. Each asset brings its own liquidity profile, pricing behaviour, and stress conditions.

This is where Sentora becomes central to the story. Its role is not just to make PRIME available on Morpho. Its role is to turn PRIME into usable DeFi collateral by defining how the vault should allocate liquidity, price risk, and protect depositors.

Sentora PRIME is therefore more than a new yield opportunity for Ethereum users. It is a case study in RWA risk design. The vault shows that private credit can be integrated into DeFi, but only when the risk is clearly identified, assigned, and actively managed. This positions vault curation as one of the most important layers in the next phase of RWA adoption.