Variational and the Shift to Onchain Brokerage

In this report, we discuss how Variational is approaching this problem through a brokerage-style model that connects traders to liquidity through RFQs, internal market making, and isolated onchain settlement.

BTC

ETH

SOL

USDC

The value leakage problem in perp markets

Perpetual futures, better known as perps, have become one of the most popular trading instruments in crypto. They account for the majority of trading activity across both centralised and decentralised exchanges.

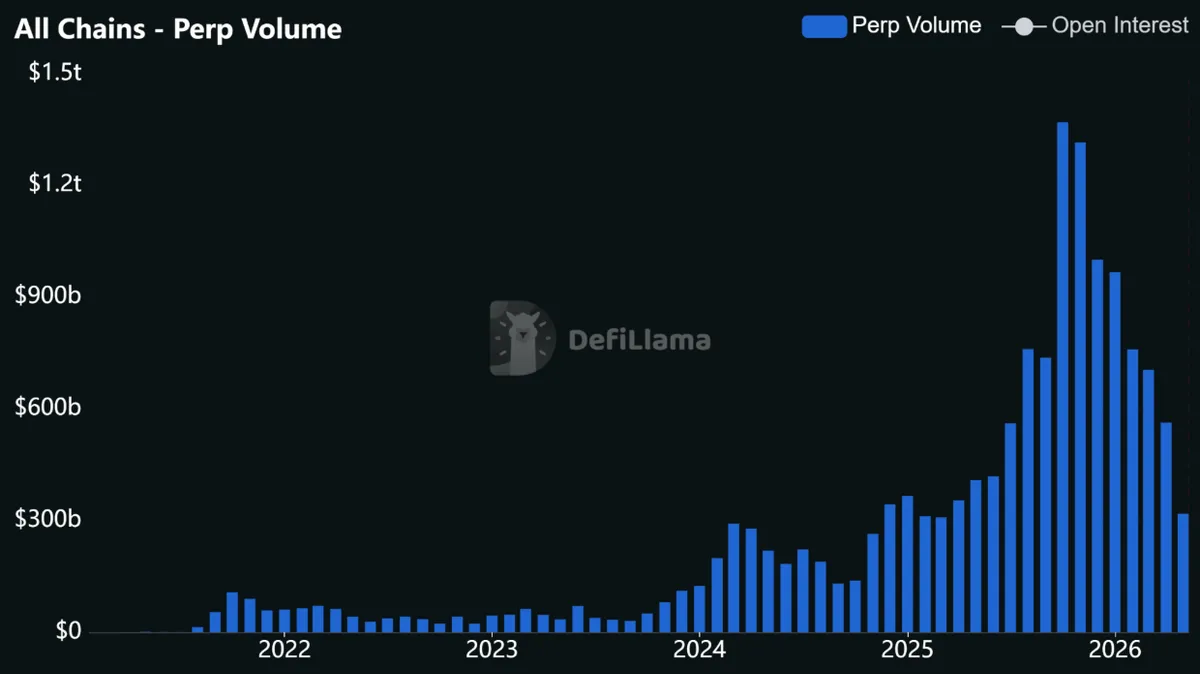

While CEXs still dominate the market, their decentralised equivalents have grown substantially over the last few years. Perp DEX volume reached $563 billion in monthly volume in April 2026, after hitting a high of $1.37 trillion in October 2025. This illustrates the significant growth of the sector, with decentralised perpetual markets now processing trillions of dollars in volume each quarter.

While perp DEXs have evolved a lot over the years and have grown relative to CEXs, both still suffer from the same underlying problem: value is extracted from traders and liquidity providers on every trade, and this value does not stay within the ecosystem.

In this section, we will show why that is the case and why a new model is needed for perp DEXs to truly shine, especially as RWA perps become a more dominant category.

The hidden cost of every trade

To understand how value leaks from perp DEXs, it helps to look beyond the headline trading fee. Traders also pay through spreads, slippage, liquidation costs, and other forms of execution friction that are less visible but can become meaningful at scale.

A venue may advertise low fees, but the real cost of execution depends on the full trade experience. If spreads are wide, liquidity is thin, or liquidations happen during volatile markets, value can be extracted from traders in ways that are not always obvious upfront.

Cost | How it appears to the trader | Who captures it today | Why it matters |

|---|---|---|---|

Trading fee | Visible fee shown by the exchange | Exchange or protocol | Easy to compare, but only part of the real cost |

Bid-ask spread | Hidden inside the execution price | Market makers or liquidity vaults | Often larger than users realize and repeated on every trade |

Liquidation cost | Forced exit during margin stress | Liquidators, venues, or counterparties | Can amplify losses when liquidity disappears |

The problem is not that these costs exist. Markets need liquidity providers, and liquidity providers need to be compensated for taking risk. The problem is where that value goes.

On most venues, trading fees accrue to the exchange or protocol, while external market makers or liquidity vaults often capture spreads. Liquidation costs are also absorbed by traders without necessarily benefiting the broader ecosystem.

The trader creates the order flow, but much of the value generated by that activity is lost instead of being recycled back into users, liquidity providers, or the protocol itself.

Why existing perp DEX models still leak value

The main reason this value leakage exists across these different costs comes down to the design choices that perp DEXs and centralised exchanges have made over time. Each model was built to solve a specific problem, but each also introduced its own trade-offs.

Centralised exchanges solved execution. They offer deep liquidity, fast order matching, and a smooth trading experience. However, users give up custody, and much of the value generated by trading activity is captured by the exchange and external market makers.

Orderbook DEXs improved custody and settlement transparency. Traders can keep control of their funds, while trades settle more transparently onchain. However, order books still often rely on external market makers for tight spreads and low slippage, meaning much of the value captured through spreads can still leave the ecosystem.

Pooled liquidity models brought more value inside the protocol by allowing users to provide liquidity directly. This helped protocols internalise more of the economics that would otherwise go to external firms. However, it also created a new problem: LPs can become directly exposed to trader PnL. When traders win, LPs can lose, which creates a more adversarial relationship between traders and liquidity providers.

Model | What it gets right | What still breaks |

|---|---|---|

Centralised exchanges | Deep liquidity, fast execution, and strong UX | Users give up custody, and value is captured by exchanges and external market makers |

Orderbook DEXs reliant on external market makers | Self-custody, transparent settlement, and better execution through professional liquidity | Liquidity still depends heavily on external firms, so spread revenue often leaves the ecosystem |

Pooled liquidity models | More value is captured inside the protocol by turning liquidity into a native system function | LPs can become exposed to trader PnL, creating misaligned risk between traders and liquidity providers |

Hybrid internal liquidity models | Some market-making revenue can stay inside the system through vaults or protocol-linked liquidity | External market makers may still compete with internal liquidity, diluting value capture |

Hybrid vault models attempt to improve on this by letting vaults participate in market making and capture some of the spread revenue internally. This can keep more value inside the system, but the model still often competes with external market makers. As a result, internal value capture remains diluted.The result is a market where every model improves one part of the system while leaving another part exposed. Some models reduce spreads but leak value to external market makers. Others internalise more value but expose LPs to trader PnL.

It has lacked a model that can combine strong execution, internal value capture, and proper risk management within the same system.

Why RWA perps expose the limits of CLOBs

Where design choices start to matter even more is with RWA perps. Demand for non-crypto perps has grown rapidly over the last year, turning them into one of the more important emerging categories within the perp DEX market.

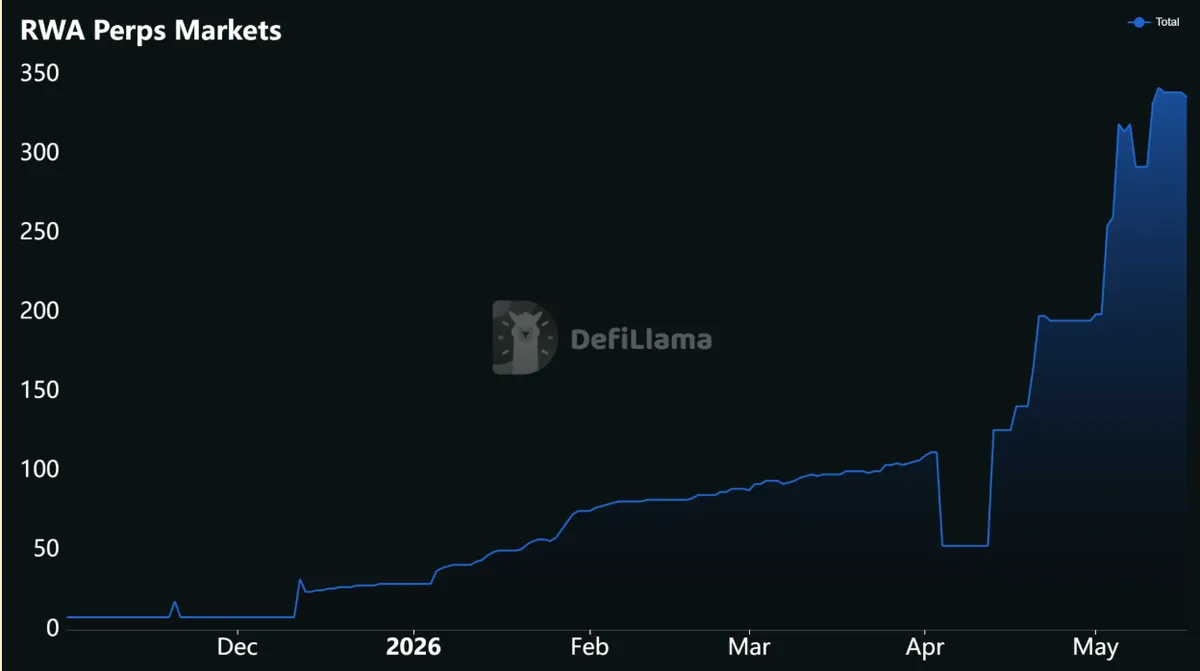

At the start of 2026, there were only 29 tradable RWA perp markets. Today, that number has reached 336, according to DeFiLlama, showcasing how much the category has grown.

This growth is also reflected in trading volumes. RWA perps went from roughly $3.6B in total quarterly volume in Q4 2025 to $121.7B in Q1 2026, a 33× increase in a single quarter. Q2 2026 is still underway, yet the category has already recorded $100.5B through mid-May, putting it on pace to match or exceed Q1 by quarter-end.

Yet with that growth comes a new set of problems. As RWA perps scale, the limits of existing market designs are becoming harder to ignore, and no design feels that tension more than the central limit order book, the dominant model across perp DEXs today.

CLOBs work best when markets already have deep two-sided liquidity. For BTC, ETH, and SOL, that condition exists. There are enough traders, market makers, arbitrageurs, and hedging venues to support active books. But RWAs are different. Stocks, commodities, indices, FX pairs, and rates already trade through massive offchain liquidity networks. Trying to rebuild that depth onchain, asset by asset, is a slow and capital-intensive path.

This is the cold-start problem for RWA trading. Every new market needs liquidity before it can attract traders, but market makers need order flow before they commit meaningful liquidity. The result is thin books, wider spreads, and worse execution. Even when a market exists onchain, it may not be deep enough to support serious size.

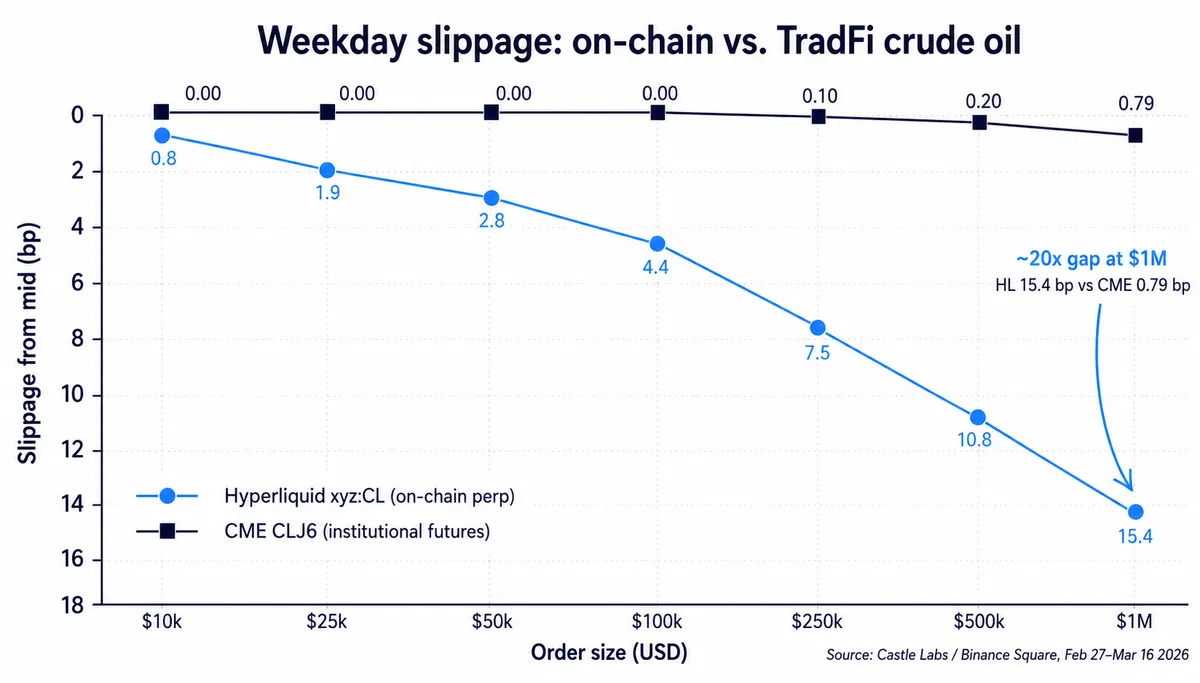

The data makes this gap concrete. Castle Labs benchmarked Hyperliquid's onchain crude oil market against CME's WTI contract and found a 20x slippage gap at $1M order sizes, with Hyperliquid clocking 15.4 basis points against CME's 0.79 basis points. Even at smaller sizes, the difference is notable as a $10k order on Hyperliquid incurs 0.8 bp of slippage while CME registers essentially zero.

This does not mean onchain RWA markets will fail. It means the design of perp DEXs supporting them has to be different. The weaknesses of CLOBs were not that notable with crypto-native markets, but are starting to show with RWAs, creating real value leakage that is harder to ignore.

Variational’s brokerage model

Two people who identified the design problems with perp DEXs early, before RWA perps were even relevant, were Variational’s founders, Lucas Schuermann and Edward Yu.

Lucas and Edward met as engineering students and researchers at Columbia University before launching Qu Capital, a quantitative hedge fund that was later acquired by Digital Currency Group to support Genesis Trading. At Genesis, Lucas served as VP of Engineering and Edward as Head of Quant Research, giving them direct exposure to large-scale crypto derivatives infrastructure, OTC trading, and institutional execution.

In 2021, they left Genesis to start Variational Research, a proprietary trading firm active across nearly every major CEX and DEX. Over the next two years, they integrated with leading trading venues, provided liquidity across fragmented markets, and ran market-making strategies at scale.

That experience gave them a clear view of the same problems outlined earlier in this report. By 2023, they began building the Variational Protocol to solve these problems directly.

Let’s now look at the model they chose and how the Variational Protocol is designed

Aggregating liquidity instead of rebuilding it

The key insight is that not every perp market needs to be built around a central limit order book. CLOBs are very good at price discovery in liquid markets. They work well when there is already deep demand, active market makers, and enough trading activity to keep spreads tight.

That model becomes harder to scale when the goal is “perps on everything.” Long-tail assets, RWA perps, niche equities, commodities, and FX pairs do not always have enough natural liquidity to support deep standalone order books. Each new market has to attract market makers, build depth, and create enough activity for traders to get good execution. This creates a cold-start problem.

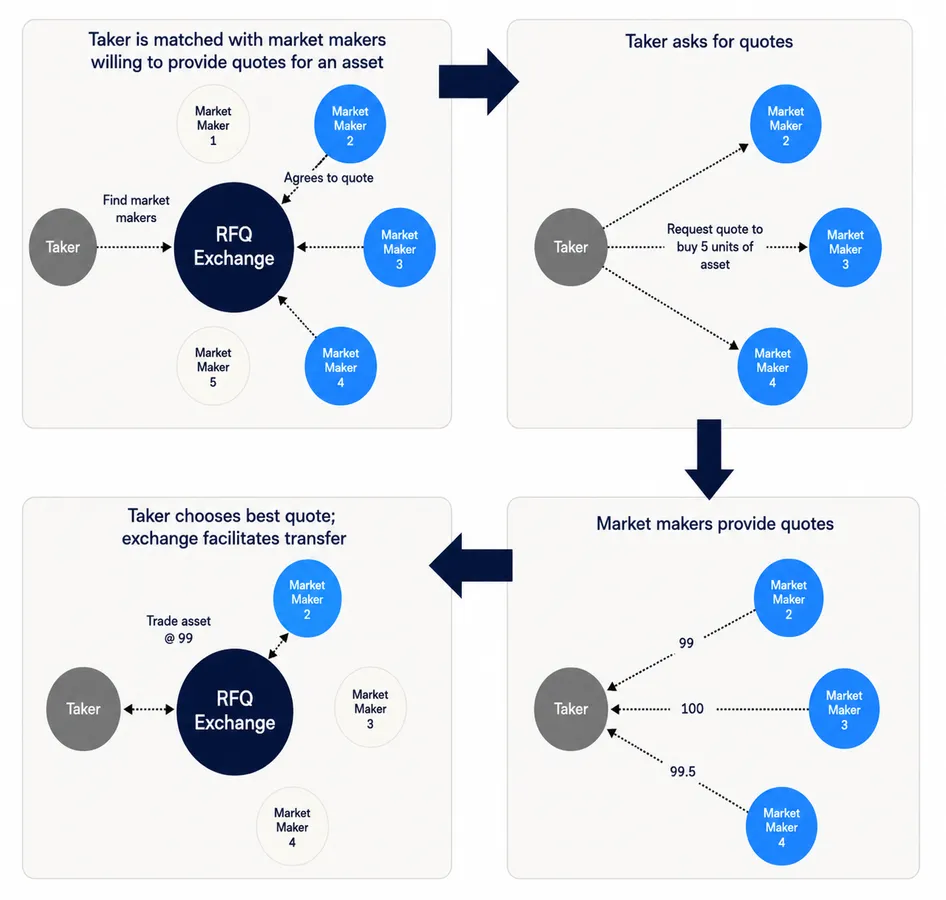

The brokerage model approaches this differently. Instead of forcing liquidity to sit inside a public order book for every market, it connects traders to liquidity through an RFQ system. RFQ stands for Request for Quote. A trader asks for a price on a specific trade, liquidity providers respond with quotes, and the trader can execute against the best available quote.

This means liquidity does not need to be bootstrapped in the same way as an order book. Instead, you can quote when there is demand, rather than constantly posting liquidity across hundreds of markets.

For perp markets, this model is especially relevant because it can support a much broader range of assets. CLOBs may continue to dominate the most liquid crypto pairs, but RFQ-based brokerage models are better suited for markets where liquidity is more fragmented, and demand is harder to predict.

The Variational Protocol stack

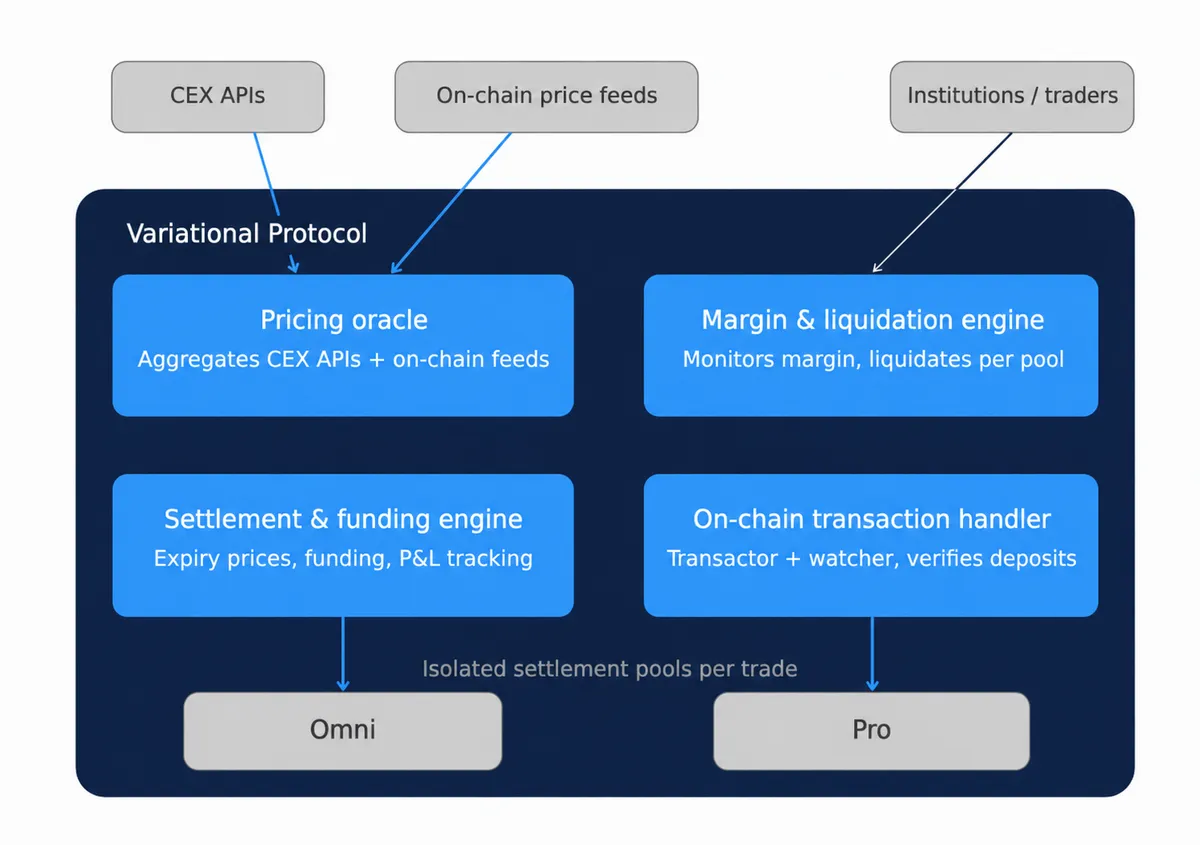

The core infrastructure where Variational's applications are built is called the Variational Protocol

The protocol is built around four core components.

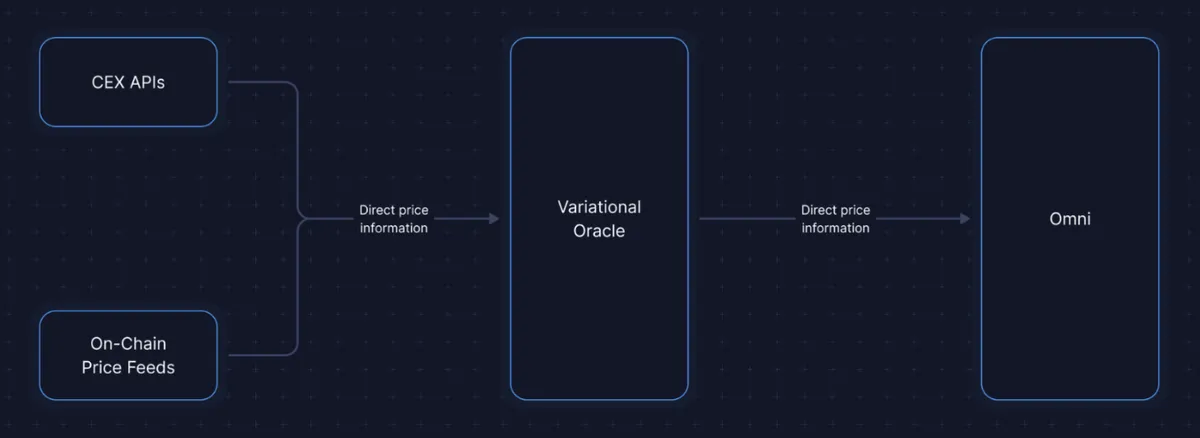

The first is a custom pricing oracle, which streams and aggregates data from a range of partnered providers across both centralised and decentralised exchanges to determine a reliable, fair value for each asset. For any asset to be tradable on Variational, the primary requirement is that dependable pricing data exists and that a consistent fair value can be derived from it.

The second is the margin and liquidation engine, which continuously monitors margin requirements across open positions and handles liquidations for any position that falls below the required threshold. Critically, this operates at the level of individual settlement pools, meaning a liquidation between two counterparties does not affect any other position elsewhere on the protocol.

The third is the settlement and funding rate engine, which determines settlement prices at contract expiration, calculates funding rates for applicable markets based on open positions, and tracks funding payments between counterparties within each settlement pool.

The fourth is the onchain transaction handler, which manages the submission and verification of all on-chain transactions. Its transactor component handles gas for user deposits and withdrawals, while its watcher component monitors whether submitted transactions have been finalised onchain, protecting against fake or incomplete deposits and ensuring that application balances always reflect actual on-chain activity.

OLP as the internal market-making layer

Built on top of the protocol infrastructure described above, the Omni Liquidity Provider (OLP) is the liquidity layer that makes trading possible on Variational.

To understand why this matters, it helps to return to the value leakage problem discussed earlier. In most venues, the exchange owns the user relationship, while external market makers provide liquidity and capture the spread. Traders create the order flow, but a large share of the economics generated by that activity leaves the platform.

The OLP changes where that value goes. Within the Variational Protocol, it acts as the direct counterparty to every trade. It quotes spreads, manages exposure, and hedges externally when needed. Instead of routing user flow to outside market makers, Variational internalises the market-making function through the OLP. Spread revenue that would otherwise leave the system can instead remain inside the protocol and be redistributed across LPs, the treasury, and other incentive mechanisms.

This makes the OLP different from earlier liquidity models. In pooled liquidity designs, depositors are often placed directly against trader PnL. When traders win, LPs can lose, which creates a more adversarial relationship between users and liquidity providers. The OLP is designed to avoid that dynamic.

Depositors contribute USDC to the vault, but their capital is not simply left as the naked other side of every user trade. Instead, the OLP functions more like an integrated market-making engine. It uses pricing algorithms, risk limits, and isolated settlement pools to manage exposure actively. When net risk builds up, it can hedge through CEXs, DEXs, OTC desks, and direct market maker relationships across venues such as Binance, Bybit, Hyperliquid, and Deribit.

This is what makes the OLP different. It is a vault that runs a sophisticated market-making strategy while also serving as the sole counterparty to user trades on Omni. At the same time, user funds remain onchain within Variational’s settlement structure and are never sent to external exchanges for hedging. OLP also posts margin in the same settlement pools as users, meaning both sides of a trade have collateral onchain and solvency can be verified.

This hedging architecture is also what makes the OLP relevant beyond crypto-native markets. Crude oil exposure can be offset through CME futures. Equity index risk can map to instruments on Nasdaq or through institutional prime brokers. FX and rates have their own deep OTC markets. The OLP is not limited to a fixed set of venues. It is designed to connect to whatever external liquidity exists for a given asset.

That means the same model that works for crypto perps can extend to commodities, equities, FX, and rates, as long as reliable pricing data and hedging routes are available.

The result is a better alignment between the three parties that any trading system depends on.

Traders get competitive execution without explicit fees. Depositors earn yield from trading activity rather than from token emissions or trader losses. The protocol captures revenue from the same flow that drives its growth.

Omni and Pro: two applications, one trading infrastructure

The protocol and the OLP are the foundation. Omni and Pro are where that infrastructure meets the market.

The two applications serve different users and different parts of the derivatives market, but they are built on the same underlying stack.

Omni

Omni is the retail-facing application. It is designed to make the brokerage model feel simple for everyday traders. Instead of interacting with fragmented liquidity, external market makers, or complex RFQ workflows directly, users trade through a familiar perp interface.

Behind the scenes, OLP acts as the integrated liquidity provider, quoting trades, managing risk, and capturing spread revenue inside the system. This is what allows Omni to offer zero-fee trading while still creating revenue for LPs and the protocol.

Omni also demonstrates one of the structural advantages of building on a brokerage model rather than an order book. Traditional venues need each market to attract its own liquidity before traders can get reasonable execution.

Omni's automated listing engine removes that constraint and makes it possible for a lot more assets to be listed on the trading platform, and it allows Omni to tap in a lot of different kinds of markets, from crypto native ones all the way to RWAs.

Pro

Pro extends the same architecture to institutions and more sophisticated counterparties. Where Omni uses the OLP as its single liquidity source, Pro opens the quoting environment to multiple market makers competing to fill each trade.

This makes it better suited to customised derivatives, larger positions, and complex products that do not fit neatly into a retail interface.

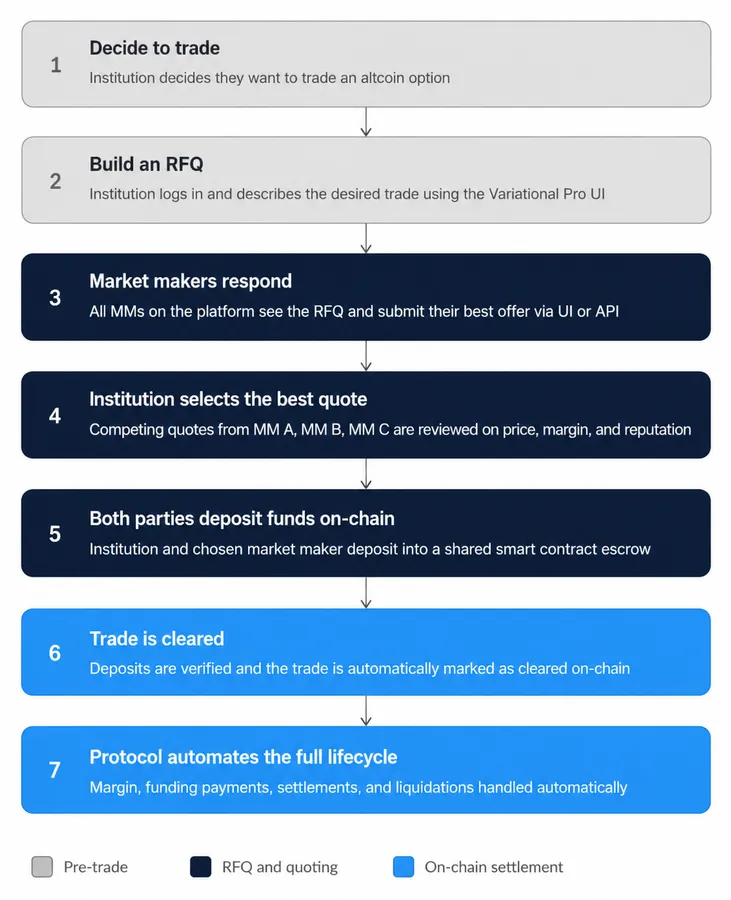

The problem Pro is solving is a real one. Institutional crypto derivatives trading still runs largely on manual OTC processes, where trades are negotiated over Telegram, margin is checked by hand, collateral moves via bank wire, and counterparty risk is managed by assumption rather than by code.

Pro replaces that with an automated onchain workflow. An institution builds an RFQ describing the trade they want, market makers on the platform respond with competing quotes, and once the institution selects the best offer, both parties deposit into a shared smart contract and the trade clears automatically. The protocol then handles margin, funding, and liquidations without any manual intervention.

This matters most for the RWA opportunity. Stocks, commodities, FX, rates, and structured products cannot be scaled through onchain order books alone, but they can be traded bilaterally if the right quoting and settlement infrastructure exists. Pro is designed to be that infrastructure, taking what is currently a fragmented and operationally heavy OTC process and making it transparent, programmable, and settled onchain.

Variational’s early traction

To understand how Variational is performing, it is important to understand the different data points behind it. For that, we look at volume and OI, spread data, the number of listings on the platform, and the revenue it has managed to generate.

Volume and open interest

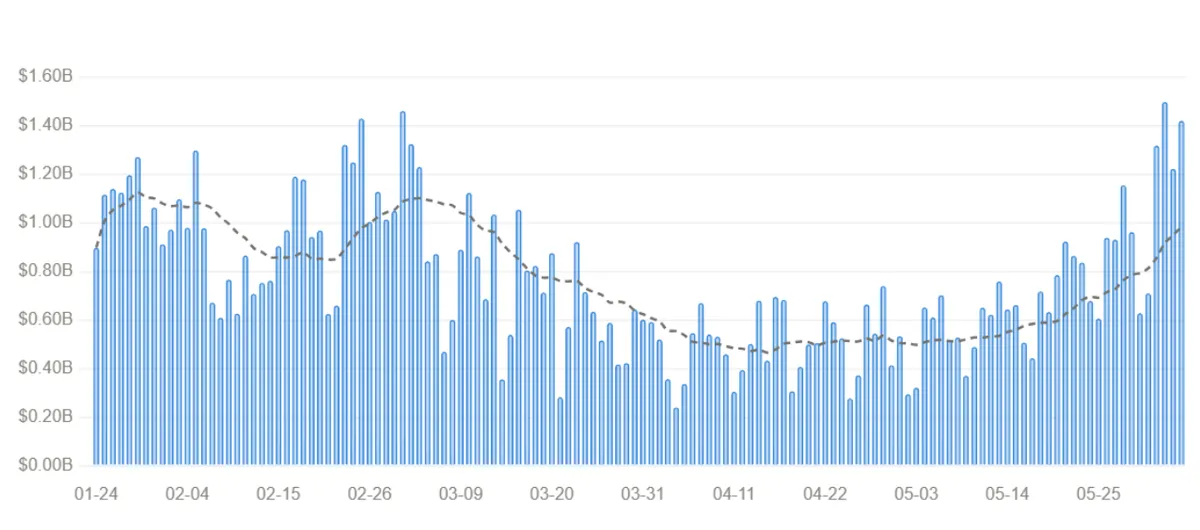

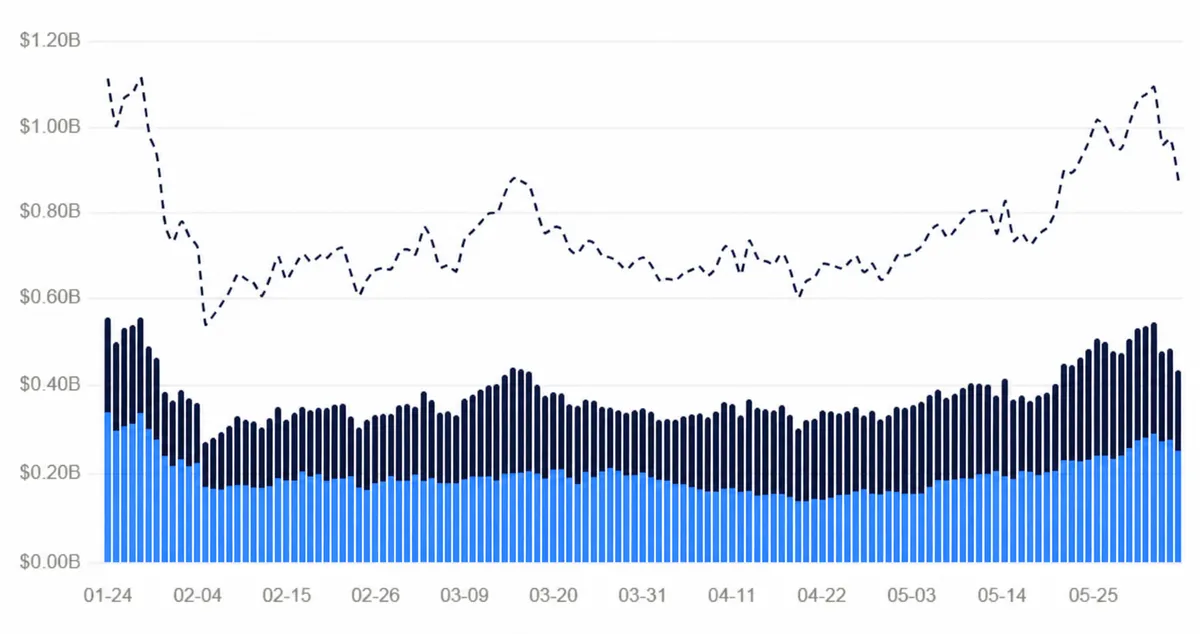

We analysed Variational's volume between January 24 and June 4, 2026, a period of 132 days, giving us a comprehensive picture of activity on the protocol.

Total volume over the period reached $100.4 billion in total notional volume, with an average 24-hour volume of $761 million per day. The single-session peak reached $1.50 billion on June 2, 2026.

Volume on Variational has been in a clear uptrend lately, with the most active cluster running from May 28 through June 4. Over those seven consecutive days, Variational recorded daily volumes above $900 million, including four sessions above $1.2 billion. June 2 ($1.50B), June 4 ($1.42B), June 1 ($1.32B), and June 3 ($1.22B) all rank among the five highest single-day sessions in the period. In the trailing 30 days ending June 4, Variational processed a cumulative $23.7 billion in volume.

Overall, Variational is showing strong and accelerating volumes that place it within the top 10 perpetual DEXs by both daily and 30-day volume, a notable achievement for a protocol at this stage and a clear signal of genuine and growing traction in the market.

Volume tells us how much activity is flowing through Variational, while open interest shows how much exposure traders are keeping open on the platform. This makes OI an important follow-up metric because it helps distinguish between short-term trading activity and more persistent usage and liquidity on the protocol.

We analysed Variational's open interest over the same period, from January 24 to June 4, 2026, covering 132 days. Average total OI across the sample was $753 million, with open interest peaking at $1.11 billion on January 24, 2026.

OI started from a strong base, with six consecutive days above $1 billion in late January, before resetting sharply in early February and reaching a low of around $504 million on February 6. After that reset, OI rebuilt steadily through March, with the strongest recovery cluster running from March 13 through March 18, when average daily OI stayed above $800 million.

From mid-May onward, OI entered a second and more sustained expansion. It crossed $800 million again around May 10 to 12, then climbed through a growth cluster from May 21 to June 1, reaching $1.09 billion on June 1, the highest level since January. Unlike the January peak, which coincided with falling volume, the June OI build occurred alongside a simultaneous volume surge, pointing to genuine position accumulation rather than stale carry.

In the trailing 30 days ending June 4, Variational maintained an average OI of $873 million, ending the period at approximately $868 million.

Together, the volume and OI data show two different sides of Variational's traction. The volume data shows that the protocol is capable of generating strong and growing trading activity, while the OI data shows that this activity is supported by a sizeable and expanding base of open positions.

Execution quality and spread competitiveness

After looking at volume and OI, the next important question is whether this activity is being supported by competitive execution quality. For a perpetual DEX, strong volume is more meaningful when traders are also receiving tight spreads, low slippage, and low total execution costs.

This is where LiquidView’s execution-cost data adds another layer to the analysis, allowing us to compare execution quality across BTC, ETH, and SOL for $10k trades.

BTC Execution Cost

For BTC, Variational is almost in line with the best available execution path. It ranks second with a total cost of 0.42 bps, only 0.05 bps behind Paradex and slightly ahead of Lighter.

Rank | Venue | Total Cost | Slip | Fees |

|---|---|---|---|---|

1 | Paradex | 0.37 bps | 0.37 bps | 0 bps |

2 | Variational | 0.42 bps | 0.42 bps | 0 bps |

3 | Lighter | 0.43 bps | 0.43 bps | 0 bps |

4 | Orderly | 1.27 bps | 0.27 bps | 1 bps |

5 | Extended | 2.58 bps | 0.08 bps | 2.5 bps |

ETH Execution Cost

The ETH market shows a similar pattern. Variational ranks second with a total execution cost of 0.50 bps, compared to 0.41 bps for Lighter.

Rank | Venue | Total Cost | Slip | Fees |

|---|---|---|---|---|

1 | Lighter | 0.41 bps | 0.41 bps | 0 bps |

2 | Variational | 0.50 bps | 0.50 bps | 0 bps |

3 | Orderly | 1.43 bps | 0.43 bps | 1 bps |

4 | Paradex | 1.64 bps | 1.64 bps | 0 bps |

5 | Extended | 2.76 bps | 0.26 bps | 2.5 bp |

SOL Execution Cost

SOL is where Variational stands out most clearly. In the LiquidView snapshot, Variational is ranked as the best execution path for a $10,000 SOL trade, with a total cost of 0.72 bps. This puts it slightly ahead of Lighter and meaningfully ahead of venues such as Paradex, Orderly, and Extended.

Rank | Venue | Total Cost | Slip | Fees |

|---|---|---|---|---|

1 | Variational | 0.72 bps | 0.72 bps | 0 bps |

2 | Lighter | 0.74 bps | 0.74 bps | 0 bps |

3 | Paradex | 1.58 bps | 1.58 bps | 0 bps |

4 | Orderly | 1.78 bps | 0.78 bps | 1 bps |

5 | Extended | 3.30 bps | 0.80 bps | 2.5 bps |

Market coverage and listing scalability

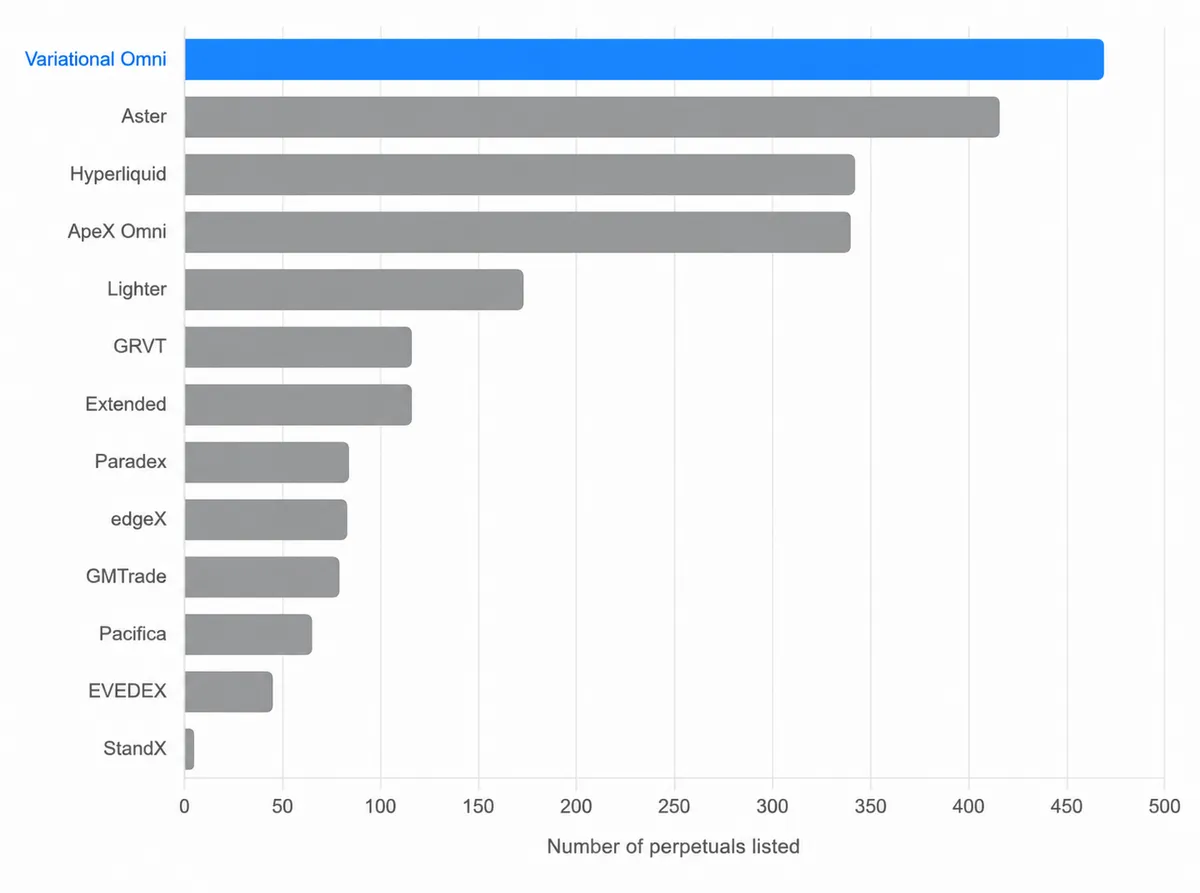

Variational’s listing count is one of the most underappreciated aspects of its model. Based on the market coverage data, Variational has the most listed assets of any perp DEX, with 469 perpetual markets. This puts it ahead of Aster with 416 markets, Hyperliquid with 342 markets and Lighter at 180 markets.

This matters because market coverage is one of the key constraints for perp DEXs. Most venues can support major assets, but listing long-tail assets is much harder. Traditional order book and AMM-based perp DEXs usually need to bootstrap liquidity, incentivize market makers, or backstop each new market before it becomes tradable. That makes broad asset coverage expensive and operationally difficult.

Variational takes a different approach. Its peer-to-peer RFQ model allows trades to be matched directly between counterparties at agreed prices, reducing the need for deep passive liquidity on every market from day one.

On Omni, new perp markets can be listed permissionlessly once they meet certain requirements, including reliable price feeds, activity thresholds, decentralization standards, and security checks. Markets can also be delisted if they no longer meet these requirements, with positions closed at a settlement price based on an exponentially weighted moving average.

Revenue capture and distribution

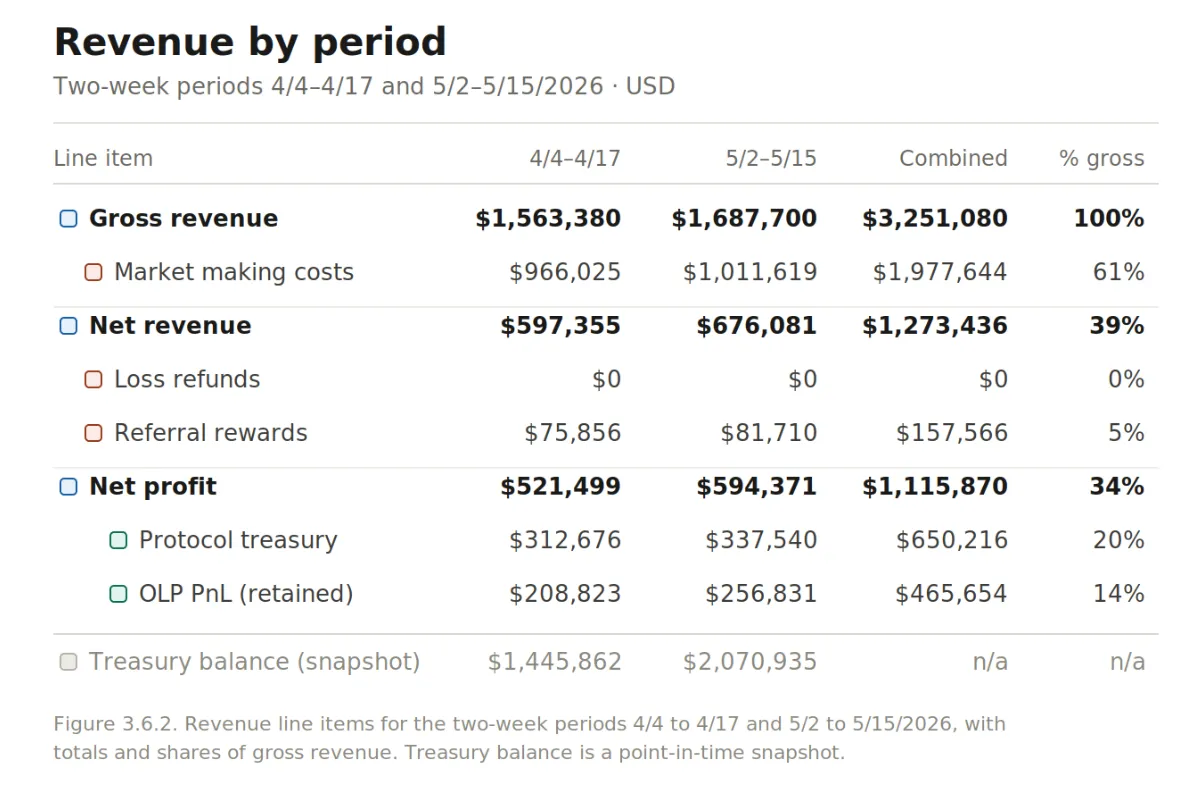

The clearest test of the brokerage model is whether the spread revenue captured by the OLP stays inside the system. Variational reports this in two-week increments, and we analysed two of them: the period from April 4 to April 17 and the period from May 2 to May 15, 2026.

Looking at two distinct periods lets us showcase the revenue flow and confirm that the distribution pattern is consistent rather than a one-off.

Across these two periods, the protocol generated $3.25M in gross revenue. Market-making cost, the expense of hedging net exposure across CEXs, DEXs, and OTC desks, absorbed $1.98M, or 61% of gross, leaving $1.27M (39%) of net revenue.

From there, loss refunds had been wound down to zero at the time, and $0.16M (5%) was paid as referral rewards, producing $1.12M of net profit, a 34% margin on gross.

Net profit split into $0.65M (20%) directed to the protocol treasury and $0.47M (14%) retained in the OLP as trading PnL.

Variational recycles roughly a third of gross revenue into the treasury and LP yield from the same flow that drives its growth. The treasury balance reflects that accumulation directly, rising from $1.45M on April 17 to $2.07M on May 15

RWA markets: from launch to early traction

On May 20, 2026, Variational listed its first four real-world assets perps: gold, silver, copper, and WTI crude. Over the following two weeks, it added seven more commodity and pre-IPO markets, including platinum, palladium, natural gas, Brent crude, and pre-IPO names such as SpaceX, OpenAI, and Anthropic, bringing the count to 11 TradFi listings by June 3.

These markets represent Phase 1 of the rollout, in which RWA perps are quoted against aggregated crypto-native liquidity rather than direct TradFi venues. It is the same approach that lets Variational list long-tail crypto markets without bootstrapping a dedicated order book for each one, now extended to commodities and equities.

The company has signaled that Phase 1 will keep expanding into equities and indices, and that any RWA market with reliable crypto-native liquidity is eligible for listing. Phase 2, slated to begin later in June, will connect directly to TradFi liquidity during market hours and eventually bring new markets onchain as CFDs, with a stated target of more than 100 TradFi markets over the summer.

Early adoption has been quick to build. Per Variational's own figures, RWA markets accounted for roughly 10% of platform trading volume since launch and about 14% of current open interest, equivalent to approximately $140M.

One of the largest single TradFi trades to date was a $2.19m SpaceX (SPCX) buy. The most telling metric may be the breadth of participation: more than 20% of active accounts had placed at least one RWA trade within the first two weeks.

For a product line only two weeks old, a roughly 14% share of open interest is a meaningful signal that demand for onchain RWA exposure is real and that Variational's listing model can capture it quickly.

Risks and mitigations

Variational’s model solves several weaknesses in existing perp DEX designs, especially around market coverage, execution, and isolated settlement. However, the same design also introduces its own set of risks.

The main risks come from oracle design, OLP’s role as the sole counterparty, smart contract execution, and the complexity of supporting long-tail or future RWA markets

Oracle risk

Variational uses its own oracle system to price the assets supported by the protocol. The oracle streams real-time data feeds for each listed market and uses a weighted combination of prices from different exchanges. This gives Variational more flexibility because it can support new assets quickly and potentially list exotic or novel markets in the future.

The tradeoff is that pricing becomes a core dependency. If the oracle is delayed, uses bad data, or fails during volatile market conditions, the protocol could quote incorrect prices. That could lead to mispriced trades, incorrect liquidations, or settlement at prices that do not reflect the real market.

OLP and hedging risk

The Omni Liquidity Provider is central to Variational’s design. OLP acts as the counterparty to every trade on Omni, while its market-making engine generates quotes and its risk-management system hedges positions to reduce directional exposure.

This creates a cleaner trading experience for users, but it also concentrates liquidity risk in one place. If OLP performs well, traders can receive tight spreads, zero-fee trading, and access to a large number of markets. If OLP performs poorly, the system can be exposed to market-making losses, hedging failures, or bad debt.

Like any market-making system, OLP can lose money, and if OLP becomes insolvent, future realized or unrealized PnL owed to users could become bad debt.

Deposits are not moved to external venues for hedging, while OLP uses its own capital for hedging activity. This limits user exposure to external exchange incidents, but OLP depositors may still face losses if hedging venues or counterparties fail.

Smart contract and settlement risk

Variational relies on on-chain settlement pools to manage collateral, margin, liquidations, and trade settlement. Each user on Omni has a bilateral settlement pool with OLP, and those pools are isolated from each other. This means positions in one pool cannot be transferred or netted with another pool, and unrelated parties cannot access funds in pools they are not part of.

This isolation is a strength because it reduces commingled risk. However, it also means the smart contracts controlling these pools are critical infrastructure. Any vulnerability in the settlement, margin, or liquidation logic could have direct consequences for user funds.

Variational has, however, taken the necessary security steps. The protocol completed audits with Zellic and Spearbit before the Omni private mainnet launch, and it also runs an Immunefi bug bounty program.

Liquidation and parameter risk

Variational’s margin and liquidation system automatically tracks whether positions have enough collateral. On Omni, liquidations occur when maintenance margin reaches or exceeds 100%, and the platform uses partial liquidations to reduce the position only as much as needed.

This design is more controlled than a full liquidation model, but it still depends on the accuracy of pricing, risk parameters, and execution during stress periods. If markets move quickly, if liquidity disappears, or if oracle prices diverge from executable market prices, liquidations may not fully protect the system.

This risk becomes more relevant for long-tail markets, where liquidity can be thinner and price moves can be more aggressive. In those markets, even well-designed liquidation rules can be tested during volatility.

Conclusion

We believe Variational is approaching the RWA perp opportunity from the right angle. Instead of trying to force every new market into a traditional onchain order book, it uses a brokerage-style model that can connect traders to liquidity where it already exists.

This matters because RWAs such as equities, commodities, FX, rates, and indices already trade through deep offchain markets, and rebuilding that liquidity onchain asset by asset is not the most efficient path.

Variational’s RFQ model, OLP market-making layer, and isolated settlement pools give it a structure that is better suited to this problem. It can list more markets without needing to bootstrap deep liquidity for each one from day one, while still keeping settlement and collateral management onchain.

The early traction supports this view. Variational has already shown strong volume, meaningful open interest, competitive execution costs, and one of the largest market coverage footprints among perp DEXs. Its ability to list hundreds of markets is especially important because RWA adoption will depend on breadth, not just liquidity in a few major pairs.

For that reason, Variational does not look like just another perp DEX competing on fees or incentives. It is building a market creation layer for onchain finance, and its architecture makes it one of the more compelling models for bringing RWAs into perp markets at scale.