Boardwalk: Closing the Gap Between Token Launches and Token Economies

Boardwalk begins with an observation that, despite being obvious in hindsight, is often ignored: creating a market is only the beginning.

BNKR

PENGUIN

Introduction

Token Launchpads solved the problem everyone could see. They made it cheap and easy to create a token, attract buyers, and establish a market. What once required weeks of coordination can now happen in an afternoon.

But as often happens with innovation, solving one problem revealed another.

Launch infrastructure has largely been built around issuance rather than long-term participation. Once trading begins, liquidity migrates to new venues, communities coordinate elsewhere, and trading volume follows the deepest pools and best execution. The token may continue to grow, but an increasing share of that activity occurs beyond the launch environment.

The token survives, but the economy around it often doesn’t. This is one of the strangest features of crypto. Enormous effort goes into creating markets, yet remarkably little attention is paid to what happens after the opening bell.

Boardwalk begins with an observation that, despite being obvious in hindsight, is often ignored: creating a market is only the beginning.

What follows is a longer and more difficult process. Liquidity has to remain. Participants need reasons to stay engaged. Value generated by the network must find its way back to the people building it. A community must become something more than a collection of traders.

The launch is only the beginning. What follows determines where liquidity settles, who captures value, how communities coordinate, and whether a project becomes more than a tradable asset.

What happens after the launch?

Inside the launch: How tokens come to market

Token launches have mostly converged around three models: bonding curves, direct AMM launches, and auctions.

Each model solves the same basic problem. It gives a new asset a market. The difference lies in the amount of structure that exists before the market opens.

Bonding curves maximize speed. A token becomes tradable immediately, and the price moves along a predefined curve as users buy and sell.

Direct AMM launches are similarly simple. A token is paired with a reserve asset in a liquidity pool, and trading commences under the initial conditions established by the issuer.

Auctions take a slower path. They separate the contribution phase from secondary trading, giving the market time to express demand before the token graduates into live liquidity.

That difference matters.

Most launchpads optimise for getting a token live. Fewer optimise for making the launch legible. When comparing launch models across demand discovery, participant visibility, sniper and bot pressure, and price formation, auctions stand out as a more mature and less chaotic model.

They give buyers time to review a token launch and avoid the reflexive or reactive price action common in bonding curve and direct AMM launches. Instead, auctions allow participants to contribute on a more equal footing, without having to worry about missing the first block of trading.

Launch criterion | Bonding curve | Direct AMM launch | Auction |

|---|---|---|---|

Demand discovery | Demand is discovered one buy at a time as users push the curve higher. This can make momentum look like durable demand. | Demand is discovered only after the pool is already live. The market tests the initial pool through live swaps. | Demand is discovered before trading begins. Contributions create a clearer signal before liquidity is seeded. |

Participant visibility | Participants can see the curve, but the launch is mostly about acting before the next buyer moves the price. | Participants can inspect the pool, but by then trading has already started. The launch and market reaction happen at the same time. | Participants can review the launch terms before contributing. The market has time to evaluate the structure before the token trades. |

Sniper and bot pressure | High. Being early on the curve is valuable, so timing and automation become part of the game. | High around pool creation. The first blocks of trading can determine early price action and reward fast execution. | Lower. Allocation is determined through the auction process, so the launch is less dependent on being first. |

Price formation | Reflexive. Price rises mechanically as buyers enter, which can amplify hype and distort early signals. | Reactive. Price forms through swaps against the pool after the token is already live. | Deliberate. The auction creates a formation period where demand is measured before the token enters live liquidity. |

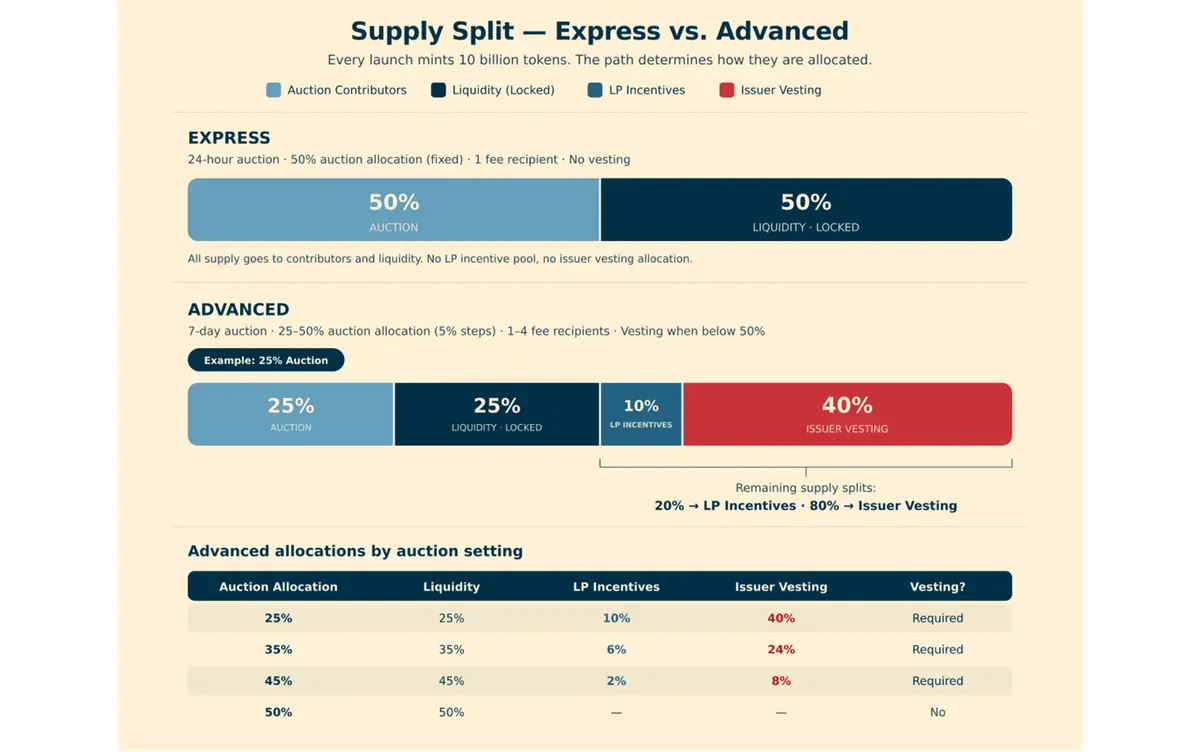

Boardwalk also saw this advantage that auctions have and designed its launch model around it. Every Boardwalk launch has a fixed total supply of 10 billion tokens, of which a percentage is up for auction.

For Boardwalk, there are two types of auctions that issuers can choose from, giving them flexibility in what type of auction they want.

Advanced: Advanced is Boardwalk’s flexible launch path. It uses a 7-day auction with a 24-hour start delay and lets issuers set the presale allocation between 25% and 50%. The same percentage is paired with the raised asset to seed liquidity, while the remaining supply becomes a vesting pool split between LP incentives and issuer-directed vesting. Advanced also supports multiple fee recipients, an optional referrer, and fixed three-year vesting.

Express: Express is Boardwalk’s simpler launch path. It uses a 24-hour auction with a fixed 50/50 split, where 50% goes to auction contributors and 50% is paired with the raised asset to seed liquidity. Express does not include vesting or a referrer. It has no LP vesting allocation, although LPs still receive the protocol-defined fee incentive stream and pool-level swap fees.

This is a smart design choice, as it allows issuers to choose between two paths. They can optimise for speed through a simpler launch, with 50% of the tokens allocated to the auction and 50% paired with the raised asset as locked liquidity. Alternatively, they can choose a longer and more structured launch that includes issuer vesting, LP incentives, multiple fee recipients, and more configuration flexibility.

Importantly, on the vesting side, the amounts, schedule, and labels are immutable once the vesting stream is initialized.

Boardwalk also rewards early contributors, but without turning participation into a pure game of speed. It does this through an early participation bonus.

Earlier contributions receive more weight inside the auction. The bonus starts at 10% at the beginning of the auction and decays to 0% by the end.

For example, a contributor who deposits 1 wETH halfway through a 7-day auction receives an approximately 5% bonus, meaning their weighted contribution is around 1.05 wETH for allocation purposes. A contributor who deposits the same 1 wETH in the final minutes receives no bonus. Both deposits still count equally toward the graduation threshold.

Overall, it is clear why an auction is a better design. It removes much of the chaos associated with bonding curves and direct AMM launches. What Boardwalk has done is add more structure and clearer paths to the auction process, while still making sure early participants can be rewarded. This makes it a vastly superior model.

Value capture after launch

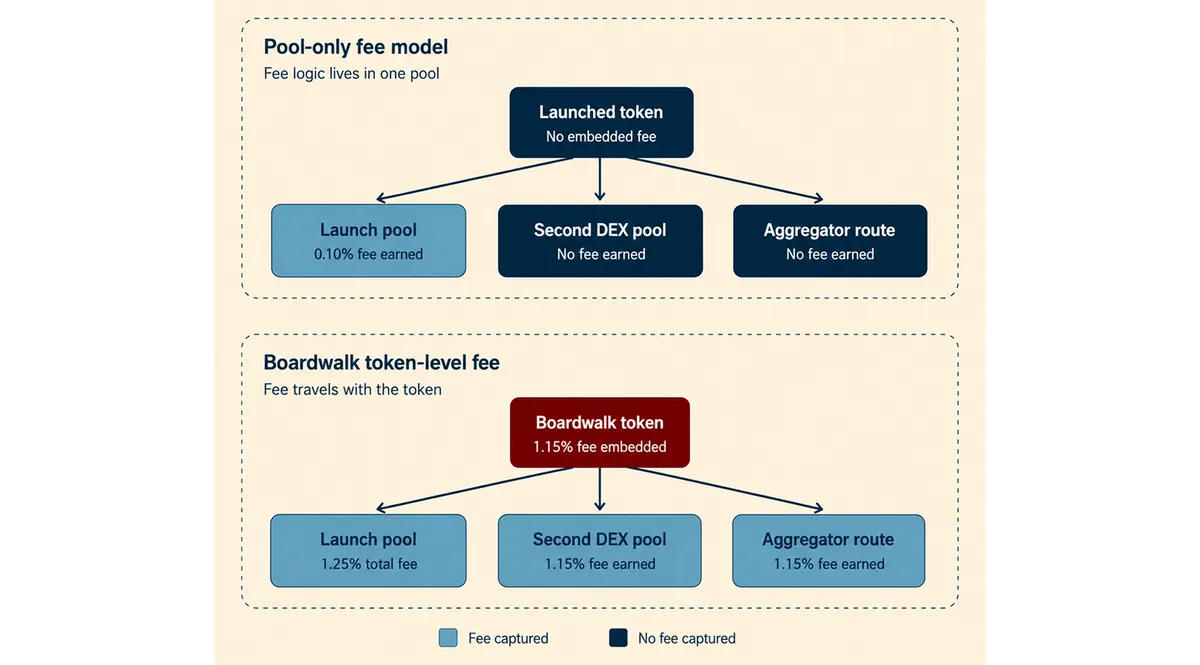

After the launch, one of the most important questions for tokens is how much creator fee revenue they can earn from their token activity, as this is often one of the first revenue streams connected to the token. However, on most launchpads, creator fees are only earned inside the launch pool and not in external liquidity pools.

This means tokens can miss out on a significant amount of potential fee revenue. We can showcase this by looking at the volumes of BNKR, which launched on the Bankr launchpad, and PENGUIN, which launched on pump.fun.

Both platforms include creator fees, but those fees are only earned inside the launch pool. When we compare launch-pool volume with external trading volume, it becomes clear how much potential revenue creators miss.

Token | Total All-Time Volume | Launch Pool Volume | Outside Launch Pool | % Outside Launch Pool |

|---|---|---|---|---|

BNKR | $2.98B | $336.6M | $2.64B | 88.70% |

PENGUIN | $2.34B | $438.3M | $1.90B | 81.30% |

For BNKR, the Uniswap V3 BNKR/WETH 1% pool on Base recorded $336.6M in onchain swap volume since launch. Total all-time volume, however, reached $2.98B across all venues. This means 88.7% of BNKR’s trading activity occurred outside the original pool.

PENGUIN followed a similar pattern. Its pump.fun bonding curve captured $438.3M in trading volume. The total all-time volume later reached $2.34 billion, indicating that 81.3% of the volume occurred outside the launch venue, primarily driven by CEX listings and secondary market activity.

This shows that tokens launched on these platforms can lose up to 80% of their potential creator fees, as trading fees instead go to LPs providing liquidity in external liquidity pools.

In Boardwalk’s case, that is not an issue because the platform embeds a 1.15% fee at the token level rather than the pool level. Unlike a pool-only fee model, this applies to non-exempt transfers, including supported external trade routes, rather than being limited to the initial pool. Taken together, this means tokens launching on Boardwalk can rely on a stronger post-launch revenue stream from their token activity.

On top of the built-in fee, Boardwalk also helps keep liquidity inside its main pool by exempting users from the token fee when they add or remove liquidity through Boardwalk. In other words, LPs using Boardwalk’s standard pools do not pay the built-in token fee on those liquidity actions.

This exemption does not apply to external pools. LPs that add or remove liquidity outside Boardwalk’s standard pools still have to pay the built-in token fee, which gives liquidity providers a stronger incentive to stay within Boardwalk’s own liquidity system.

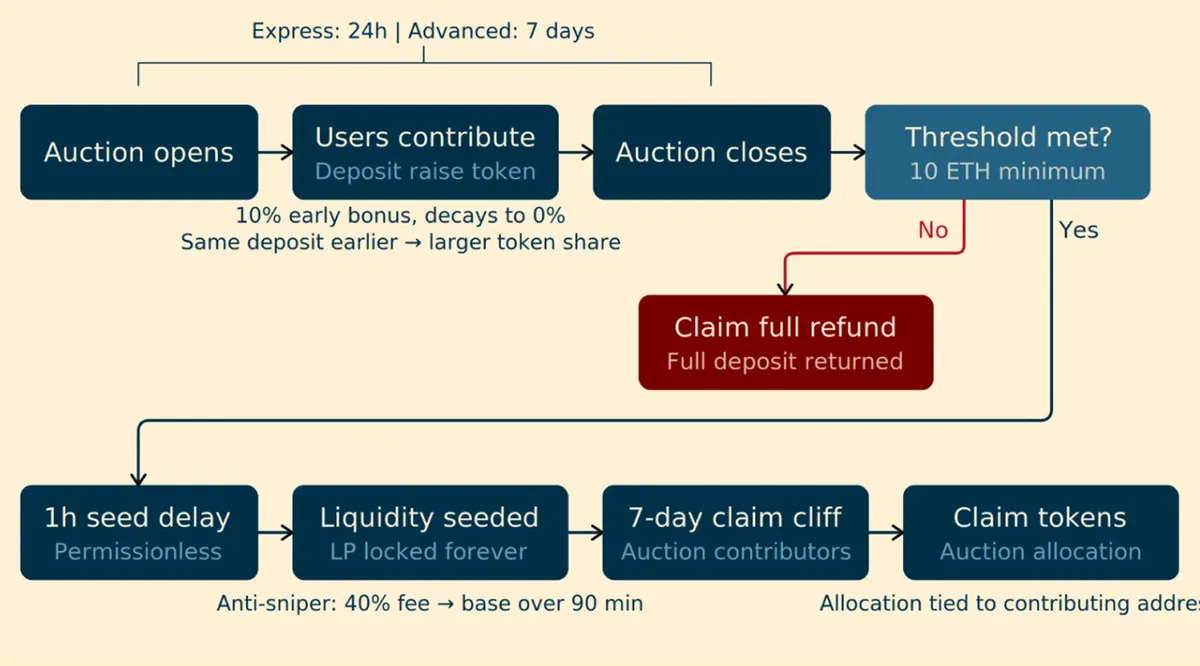

Beyond that, Boardwalk has also made several other improvements to existing launch models. The token is seeded with permanently locked liquidity, and the platform also includes anti-sniper protection for the launch pool.

Right after liquidity is seeded, the anti-sniper window begins. The fee starts at 40% and decays down to the token’s base fee over the first 90 minutes after launch. After that, the base fee applies permanently.

When you look at the entire lifecycle, it becomes clear that Boardwalk’s model creates a healthier environment for projects to launch. Projects can rely on a fee stream based on post-launch volume, while contributors benefit from a more structured launch process that gives them greater confidence to participate.

Fee routing: From extractive to positive sum

How a launchpad earns fees is one part of the model. Where those fees go is just as important.

One of the main criticisms of launchpads is that they are often viewed as extractive. While they benefit from a wide range of infrastructure, including the chain they launch on and the surrounding ecosystem, fee routing often only includes a narrow group of participants.

In a typical launchpad model, the creator earns fees, the launchpad itself earns fees, and LPs earn fees. In some cases, fees may also flow to native token stakers or other incentive programs. Overall, however, only a narrow group tends to benefit from the launch.

Token creator or issuer | Receives a share of trading fees or launch-related revenue. | Aligns the creator with token activity, but does not necessarily fund the wider ecosystem around the token. |

Launchpad or protocol treasury | Captures protocol revenue for operating the launch venue. | Can make the launchpad look extractive if most value accrues to the platform. |

LPs or liquidity venue | Earn swap fees from the pool where trading happens. | Fee capture can move away from the launch environment once liquidity fragments across other venues. |

Token holders or stakers | In some models, fees support token holders, stakers, or token-owned liquidity. | Can improve holder alignment, but still usually keeps the fee loop inside the protocol itself. |

Boardwalk has designed its fee routing in a way that more closely supports an economy rather than extracting from it. This is clear from the number of possible recipients that can participate in fee flows during a Boardwalk launch.

Boardwalk fee destination | Amount | Why it matters |

|---|---|---|

Issuer and issuer-designated recipients | 0.30% on Arbitrum, Base, Katana, and Fraxtal. 0.35% on Ethereum. | Gives the project a recurring revenue stream and lets issuers route fees to treasuries, contributors, vendors, or other aligned participants. |

Referrer | 0.05% on Advanced launches. If no referrer is set, this portion defaults to Boardwalk. | Rewards discovery and distribution when a referrer helps bring a launch into the ecosystem. |

Boardwalk | 0.30% on Advanced launches. 0.35% on Express launches. | Funds the protocol layer that operates and maintains the launch infrastructure. |

LP incentives | 0.23% on Arbitrum, Base and Katana. 0.25% on Fraxtal and Ethereum. | Gives LP Participants a dedicated fee stream on top of normal pool swap fees. |

Integrators, chains, and ecosystem partners | 0.27% on Arbitrum, Base and Katana, 0.25% on Fraxtal, and 0.20% on Ethereum. | Connects token activity to the chains, infrastructure providers, data providers, security partners, and public goods that support the launch environment. |

DEX-level swap fee | 0.10% across all chains. | Accrues through the standard v2-style pool and supports normal pool economics. |

To start, the idea of issuer-designated recipients, on top of the issuer being able to generate fees, is extremely innovative. It moves selected economic participants directly into the money flow of the economy. As Jason Rosenthal from a16z crypto describes it, some of the strongest businesses are built by sitting where value moves and taking part in that flow. Boardwalk applies that concept at the token launch level by allowing projects to route part of their ongoing fee stream to selected recipients.

The key point is that revenue scales with usage. If a token economy attracts more trading activity, the fee stream grows with it. This means projects launching on Boardwalk can negotiate with vendors, such as auditors, before launch and offer them a share of future fees instead of only paying a fixed upfront fee.

The same logic applies to advisors, referrers, and other launch participants. Fee percentages are fixed once set. The referrer allocation and percentage are immutable, though the referrer can rotate its own recipient address through a typed, seven-day timelocked process.. The same distinction applies to issuer-recipient slots: the economic entitlement is fixed; the specified address can rotate. This preserves the agreed economics while giving issuers flexibility if vesting relationships change, performance declines, or vesting allocations should be redirected to other partners or public goods.

Another innovation Boardwalk introduced is the integrator fee, which supports the chains that Boardwalk is live on, as well as 0x, the DEX aggregator that Boardwalk has partnered with. This ensures that ecosystem partners also benefit from the launches happening in their ecosystem.

Chain | Integrator allocation | Recipients |

|---|---|---|

Arbitrum | 0.27% | 0.25% to the chain and 0.02% to 0x. |

Ethereum | 0.20% | 0.08% to Sherlock, 0.05% to a security public good, 0.05% to DeFi Llama, and 0.02% to 0x. |

Base | 0.27% | 0.25% to the chain and 0.02% to 0x. |

Fraxtal | 0.25% | 0.25% to the chain. |

Katana | 0.27% | 0.25% to the chain and 0.02% to the Boardwalk Operations Reserve until 0x integration. |

Ink | 0.27% | 0.25% to the chain and 0.02% to 0x. |

In the case of Ethereum, the integrator fee goes to security auditor Sherlock, DefiLlama, and Security Alliance (SEAL). Through a reciprocal arrangement, teams launching on Boardwalk receive a 30% discount on Sherlock’s full suite of security services in year one, reducing to 20% in subsequent years. The discount covers collaborative audits, audit contests, Sherlock AI, and bug bounty programs.

Overall, this integrator fee clearly shows that Boardwalk is trying to play positive sum games. It is trying to build economies on top of it, where the chain and ecosystem partners also benefit from the launches that happen on Boardwalk.

Coordination after the first trade

While fee capture and fee routing are important, another key post-launch issue is coordination. This is also where many launchpads face problems.

Most launchpads have a page showcasing the token and its profile, but coordination is often extremely fragmented and depends on each project. Some projects move their community to Discord, others use Telegram, and some post updates on X. Others may decide not to have much presence on X at all.

For users, it is also not always easy to track which launches they have participated in or to view a unified dashboard of their activity on the platform.

Boardwalk solves this coordination gap through two dedicated layers: Café Boardwalk and the Dashboard.

Café Boardwalk: The public town square

Café Boardwalk is the community space attached to every launch. It gives issuers, contributors, LPs, and third parties a public place to discuss the token, ask questions, share updates, and coordinate around the project after launch.

Unlike a private Discord or Telegram group, Café Boardwalk sits on the open web. This makes each economy easier to discover and provides new participants with a place to understand what is happening before they invest energy into the project.

Issuers can use their launch’s space to post updates, answer questions, and share context that did not fit on the launch page. What makes Café Boardwalk different is that it is not only a place for issuers to post content. It also serves as a coordination layer where discussions can occur and third parties can connect with the project.

This includes parties that want to support a token through liquidity support, growth and community help, security review, treasury management, or public-good contributions. Instead of coordination happening across fragmented channels, Café Boardwalk gives each token economy a shared public space where issuers, contributors, and service providers can stay connected.

The Dashboard: The control room

Boardwalk also gives users an account-level dashboard to track their activity across the platform. It shows auctions joined, tokens launched, total contributions, claimable balances, liquidity positions, BWS staking, visibility influence, and fee or vesting allocations.

This is useful because participation does not end after the auction. Users may have tokens to claim, LP positions to manage, BWS staked, or fees and vesting allocations across multiple launches. The dashboard brings these actions into one place.

For issuers, the dashboard also tracks launches they have created, including total raised, current status, key milestones, and the next available action. This gives both users and issuers a clearer view of their role in the Boardwalk economy.

BWS: A launchpad token built for consumption and fee direction

Most launchpad tokenomics are still fairly simple. They usually revolve around access, staking, fee sharing, buybacks, or governance. These mechanisms are easy to understand, but they can also introduce weaknesses

Access models only give the token utility when there is enough demand for launches on the platform, but they often lack utility beyond that. Fee-sharing and buyback models are more compliance-sensitive because they can turn the token into a yield product, or into something users hold with the expectation that revenue will be routed back to the token. Governance models can also be compliance-sensitive, as they give token holders control over parts of the platform.

Launchpad token model | How it usually works | Main limitation | Compliance sensitivity |

|---|---|---|---|

Access and allocation token | Users hold or stake the token to qualify for launches, enter tiers, or improve allocation chances. | Utility depends heavily on a constant pipeline of attractive launches. If launch quality slows down, token demand can weaken quickly. | Can become sensitive if users mainly hold or stake because they expect access to profitable future launches. |

Fee-sharing token | Token holders or stakers receive a portion of launchpad fees, trading fees, or platform revenue. | Easy to understand, but it can turn the token into a passive yield product rather than an active utility asset. | Higher sensitivity because holders may appear to expect profits from platform activity or the work of the launchpad team. |

Buyback and burn token | Platform revenue is used to buy the token from the market and burn it. | Cleaner than direct fee sharing, but still ties token value mainly to platform revenue rather than direct usage. | Lower than direct fee sharing in some cases, but still sensitive if marketed as a value-accrual mechanism for holders. |

Governance token | Token holders vote on launch approvals, fee policies, treasury spending, or platform decisions. | Governance is often broad, vague, or has low-participation, and may give holders more control than is needed. | Can become sensitive if governance gives holders control over revenue, treasury assets, or core protocol operations. |

Boardwalk has taken a different approach with BWS. Instead of using a conventional launchpad token model based only on access, fee sharing, buybacks, or governance, BWS is designed as a utility and consumption token with a more narrowly defined role inside the protocol.

The first role is consumption. BWS is burned when users perform specific actions on Boardwalk. Issuers burn a protocol-defined amount of BWS to launch a token economy. Users also burn BWS when they Upvote or Downvote tokens and auctions in discovery. Each address can use one Upvote and one Downvote per token or auction every 30 days, making these signals a recurring but limited action

This is a useful mechanism as it makes discovery more intentional. Instead of visibility being driven only by passive attention or low-cost engagement, users have to burn BWS to signal conviction. Projects that receive more Upvotes, therefore, show that users are willing to spend BWS to improve their visibility. This helps Boardwalk surface launches with stronger community interest and makes it harder for discovery to be driven only by spam.

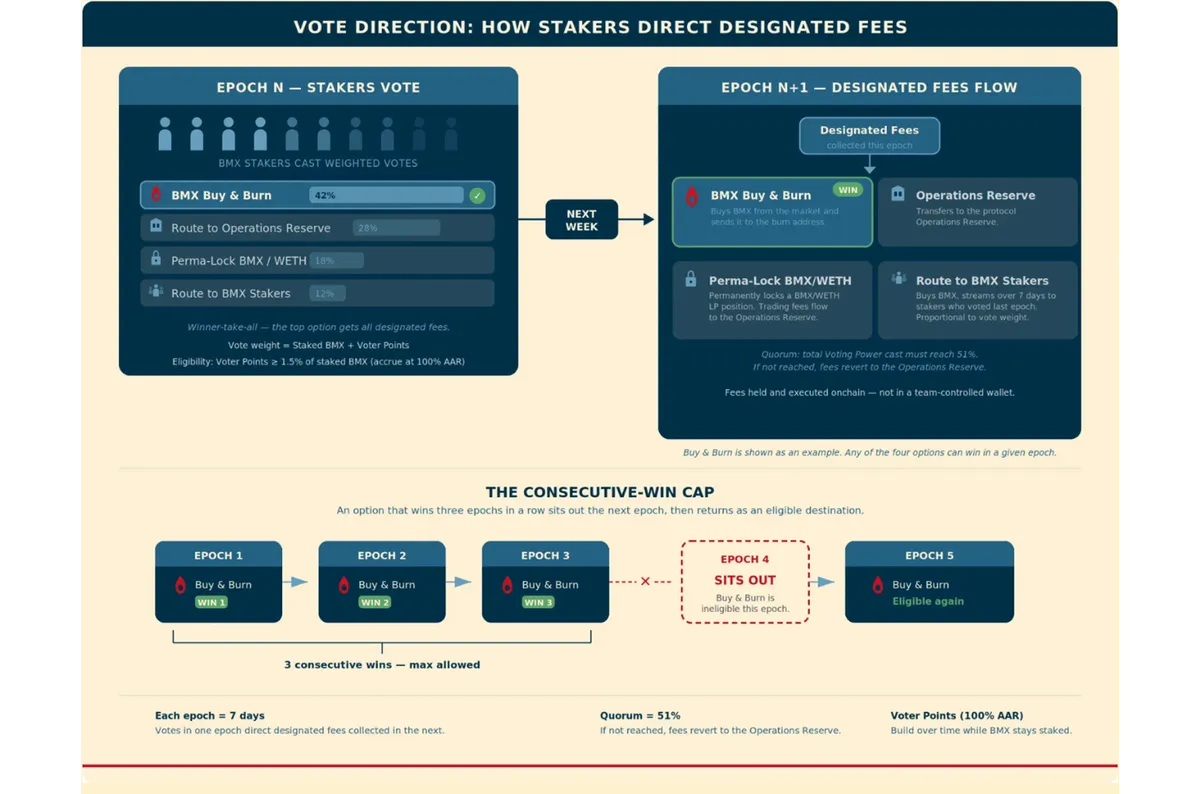

The second role is staking and fee direction. Holding BWS and staking BWS are separate actions. Holding BWS lets users use the token for launch creation and community signaling, while staking BWS creates eligibility to participate in Boardwalk’s fee-direction system.

Boardwalk’s voting system is based on Voting Power, which equals staked BWS plus Voter Points. Staked BWS forms the base of a user’s voting weight, while Voter Points accrue at a 100% annual rate for as long as the BWS remains staked. These points are non-transferable, have no market value, and burn proportionally when a user unstakes.

The reward for duration is greater influence over fee-direction voting. A user who keeps BWS staked for longer can build more Voting Power than someone who stakes the same amount for a shorter period. This is a smart design choice because it rewards longer-term participation without creating a separate liquid points market or turning points into a tradable asset.

Voting takes place in weekly epochs. During each epoch, BWS stakers vote on where a designated portion of Boardwalk’s fees should be routed in the following epoch. The vote is winner-take-all, and the winning outcome is executed automatically by the protocol’s contracts. The designated fees are held onchain by the protocol rather than in a team-controlled wallet.

Boardwalk currently gives stakers four routing options:

Option | Outcome |

|---|---|

Buy and Burn | Fees are used to buy and burn BWS |

Operations Reserve | Fees are routed to the Operations Reserve |

Lock Liquidity | Fees are used to permanently lock BWS/WETH liquidity |

Staker Stream | Fees are used to buy BWS and stream it to eligible stakers over seven days |

The system also includes several constraints that reduce capture and prevent the same outcome from dominating indefinitely. To vote, a staker needs Voter Points equal to at least 1.5% of their staked BWS. Boardwalk also uses a 51% quorum, meaning total Voting Power cast must reach at least 51% of the snapshotted total. If quorum is not reached, the designated fees default to the Operations Reserve for that epoch.

Finally, any option that wins three epochs in a row becomes ineligible for the next epoch. After sitting out one epoch, it returns to the ballot. This prevents a single fee route from winning indefinitely and forces periodic rotation between burn, liquidity, operations, and staker distribution outcomes.

These constraints are what make BWS less exposed to the compliance sensitivities that usually come with fee-sharing or staking tokens. Stakers do not receive a fixed claim on protocol revenue, and staking BWS does not automatically create a guaranteed recurring yield stream. Instead, stakers participate in a limited fee-direction process where a defined portion of fees is routed through weekly votes and fixed onchain options.

BWS stands apart from most launchpad token designs. Instead of creating demand mainly through access, passive yield, or governance, BWS ties participation to specific actions inside Boardwalk.

Users burn it to launch and signal conviction, while stakers use it to direct a defined portion of fees through fixed onchain options. This makes the model more nuanced and less compliance-sensitive than conventional launchpad token designs.

That makes the design more limited by intent, but also cleaner. BWS is useful without giving holders control over the protocol or turning the token into a simple revenue claim. For a launchpad trying to build more structured and compliance-oriented token economies, that is a stronger design choice than the conventional models that we have seen in the past.

Immutability and compliance-oriented design

Immutability is one of the most important parts of launch infrastructure because a token launch is built on trust at the moment when information asymmetry is highest. Contributors enter before the market is live, LPs take exposure before trading history exists, and service providers may agree to support a project before there is a stable revenue stream.

In that environment, the question is not only what the launch terms are. The question is whether those terms can change later.

This matters from a compliance perspective as well. Crypto regulation often focuses on disclosure, control, expectations, and the role of an active party after launch. If key economics can be changed after users participate, the launch depends more on the issuer or platform's discretion. If the core terms are fixed, visible, and enforced by contracts, the structure becomes easier to understand and less dependent on offchain promises.

Compliance-oriented principle | Why it matters for token launches |

|---|---|

Predictable economics | Users can evaluate fees, supply, vesting, and liquidity before participating, instead of relying on future decisions by the issuer or platform. |

Reduced discretion | The fewer things an issuer or admin can change after launch, the less the economy depends on ongoing managerial control. |

Clearer disclosures | Immutable terms are easier to document because the rules participants see before launch are the rules that apply after launch. |

Lower trust assumptions | Timelocks, fixed supply, locked liquidity, and non-upgradeable contracts reduce the need to trust that privileged parties will not change the system later. |

This is where Boardwalk’s design stands out. The platform not only makes sure launches are structured. It documents, at the contract level, what is immutable, what can still change, and which changes are limited to future launches.

For live launches, the core economics are fixed. Fee percentages are set when the launch is created. Factory-level defaults can change for future launches, but those changes do not rewrite launches that are already live. Vesting amounts, schedules, and labels are also immutable once the vesting stream is initialized. Only the recipient address can change later, and that follows a timelocked path.

Boardwalk also limits post-launch trust around supply and liquidity. Every launched token has a fixed supply of 10 billion tokens. After the initial mint at liquidity seeding, no more tokens can be created. The seeded LP tokens are burned to the dead address, which means the initial liquidity position cannot be withdrawn by an issuer, admin, or team wallet.

Area | Boardwalk design | Why it matters |

|---|---|---|

Fee schedule | Live-launch fee percentages are fixed at creation. Future factory changes only affect future launches. | Participants can rely on the fee structure they reviewed before entering. |

Vesting | Vesting amounts, schedules, and labels are immutable once initialized. | Issuers cannot rewrite unlock terms after the market has formed. |

Supply | Each launched token has a fixed supply of 10 billion tokens and no open mint path after seeding. | Removes later inflation risk from the issuer or protocol. |

Liquidity | Seeded LP tokens are burned to the dead address. | The initial liquidity position cannot be withdrawn after launch. |

Upgrades | Boardwalk does not use an upgradeable proxy pattern for live launches. | Launch contracts cannot be upgraded into a different design after users participate. |

Admin powers | Several key contracts have no admin functions after initialization. Existing admin actions are timelocked. | Reduces discretionary control and gives users time to observe pending changes. |

This level of documentation is unusual for a launchpad. Many launch systems explain the user flow, the fee model, or the launch mechanics, but they do not always provide a clear inventory of what can and cannot change after launch. Boardwalk’s technical appendix does this directly. It explains the per-launch contracts, shared protocol contracts, immutable settings, timelock model, admin function inventory, contracts with no admin surface, and the maximum impact of a compromised owner key.

That last point is especially important. Even in a worst-case scenario where a protocol owner key is compromised, the impact on live launches would be limited.

An attacker could signal changes to future-launch defaults, treasury or keeper addresses, or certain voting parameters, but these actions are timelocked and publicly visible onchain before they can take effect. They could not rewrite the economics of an existing launch, mint new tokens, recover locked liquidity, bypass the token’s transfer fee, or drain user funds from staking and vesting contracts. The main exposure is therefore limited to settings that affect launches not yet created and protocol-level addresses that can only be changed after a public delay.

Overall, Boardwalk has one of the clearest documentation standards and one of the most immutable contract designs in the launchpad market. Its design makes the launch process more compliance-oriented by giving issuers and contributors clearer terms before capital enters the system

In a market where launches often depend on trust, Boardwalk makes the terms of each economy more visible, more durable, and harder to change after participation begins.

Competitive landscape: Where Boardwalk sits in the launch infrastructure market

The launchpad market is not short on alternatives. Most platforms solve one specific part of the token launch problem well. Some optimise for speed, some for liquidity, some for curated fundraising, and some for vertical-specific launches such as AI agents. The issue is that most of these models stop at launch or focus on only one part of the lifecycle.

For this section, we analysed Boardwalk against Baseline, Pump.fun, MetaDAO, Bankr, Virtuals, and Uniswap Liquidity Launchpad. Each platform has a clear strength, but most focus on one part of the token lifecycle rather than the full economy.

Platform | Chain or ecosystem | Launch model |

|---|---|---|

Boardwalk | Ethereum, Base, Fraxtal, Katana, Ink, Arbitrum | Auction-based launch with liquidity seeding after graduation |

Baseline | Ethereum and Base | Direct AMM launch into the Baseline Market Maker |

Solana | Bonding curve launch with migration to PumpSwap | |

MetaDAO | Solana | Fixed-supply pro-rata USDC sale with a discretionary cap |

Bankr | Base | Direct launch into a Uniswap V4 pool |

Virtuals | Base, Solana, Ethereum | Bonding curve launch with graduation to Uniswap V2 liquidity |

Uniswap Liquidity Launchpad | Ethereum, Unichain, Base, Arbitrum | Continuous Clearing Auction with Uniswap V4 liquidity seeding |

The table above already shows the first major difference. Boardwalk and Uniswap Liquidity Launchpad are the only platforms in this comparison built around auction-based price discovery.

Pump.fun and Virtuals utilise bonding curves, while Bankr and Baseline launch directly into AMM-style liquidity. MetaDAO, on the other hand, employs a fixed-price contribution process. This matters because auctions create a dedicated formation window before the token trades. Bonding curves and direct AMM launches are weaker models because they make price discovery reactive or reflexive and reduce the structure around the launch.

The second difference is what happens after launch. A launch model can get a token live, but that does not mean it creates a durable token economy. This is where the feature comparison becomes more important.

Feature | Boardwalk | Baseline | MetaDAO | Bankr | Virtuals | Uniswap Liquidity Launchpad | |

|---|---|---|---|---|---|---|---|

Permissionless launching | ✓ | ||||||

Auction-based price discovery | ✓ | ||||||

Standardised launch terms visible before contribution | ✓ | ||||||

Protected fee routing inside the token | ✓ | ||||||

Creator fee sharing | ✓ | ||||||

Launch fee or tax to discourage sniping | ✓ | ||||||

Native vesting or founder unlock controls | ✓ | ||||||

Onchain fee-direction | ✓ | ||||||

Integrated community coordination | ✓ | ✗ | ✗ | ✗ |

The feature comparison makes the main gap clear: most launch platforms are too narrow. They may help a token go live, but they all lack the features needed to support a full economy

Baseline’s weakness is that it is more liquidity infrastructure than a launch infrastructure. Its floor-price design means part of the liquidity is reserved for downside support instead of being fully deployed into active market depth. This can slow liquidity growth and does not solve auction-based formation, protected fee routing, fee-direction, or community coordination.

Pump.fun optimises almost entirely for speed. Its bonding curve model makes tokens instantly tradable, but it also turns price discovery into a timing game. Early buyers and bots can dominate the launch, while deeper launch terms, vesting, protected fee routing, and post-launch coordination are largely absent.

MetaDAO has the opposite limitation. Its fixed-supply pro-rata USDC sale with a discretionary cap gives contributors clearer terms, but the model is curated and less permissionless. It is closer to structured fundraising than an open launchpad and does not offer permissionless launches like the other platforms in this comparison.

Bankr focuses mostly on deployment. It makes token creation simple, but the model does not provide auction-based formation, protected token-level fee routing, onchain fee-direction, or a coordination layer after launch.

Virtuals has more launch features than most platforms, but it is still built around one vertical and relies on a bonding curve launch model. Its focus on AI-agent tokenisation limits its broader use case, while auction-based formation, protected token-level fee routing, onchain fee-direction, and a native post-launch coordination layer remain absent.

Uniswap Liquidity Launchpad stands out for its Continuous Clearing Auction, but its main trade-off is complexity. The design leaves many variables in the hands of issuers, including floor price, duration, issuance schedule, auction steps, graduation thresholds, validation modules, tick spacing, liquidity strategy, and post-auction pool setup. This flexibility can be useful for sophisticated teams, but it makes the launch harder for ordinary contributors to evaluate.

This is where Boardwalk stands apart. Other platforms leave major gaps around fee capture, fee routing, LP incentives, issuer-designated recipients, community coordination, and immutability. Boardwalk brings these pieces together into one launch standard, creating a standardized way to turn token launches into durable economies that are simple to use, but still have the features needed to be sustainable.

The Boardwalk Standard

The launchpad market has historically been built around speed. The goal was to get tokens live quickly, but that often meant the actual economy around the token was left underdeveloped. Boardwalk sets a different standard by treating the launch as the starting point for a durable market, not the end product.

The Boardwalk Standard brings together auction-based formation, locked liquidity, built-in fees, protected fee routing, vesting, LP incentives, community coordination, BWS utility, and documented immutability. This gives issuers a clear framework to define how their economy works before the market opens and keep those rules intact after launch.

This also changes how distribution works. Boardwalk does not endorse, promote, or select winners. Instead, it gives every issuer a standardized, visible, and permissionless launch surface where contributors, LPs, vendors, chains, and communities can evaluate the economy directly. Distribution comes from transparent mechanics, public launch pages, Café Boardwalk, and immutable onchain rules rather than discretionary gatekeeping.

The result is a more complete model for token formation. Issuers get a stronger post-launch revenue structure, contributors get clearer terms, LPs get more recognizable incentives, and service providers can be placed directly into the economy’s fee flows. As usage grows, the value flowing through the token economy can grow with it, giving Boardwalk a more durable and aligned launch model than the speed-first platforms it competes against.